Talking Points

- Sterling survived another year of living dangerously

- Consensus is optimistic, and so most investors are too crowded into US technology investments. Will it be another good year?

- We also welcome Helen Thomas of BlondeMoney as the regular commentator on all things geopolitical.

- Helen highlights the risks around the US midterm elections, legal challenges to Trump’s tariff policy, and France’s ongoing political problems.

- She is not optimistic about Starmer’s chances for surviving 2026

Year-End Review

First, I want to thank you for your trust and your business. We could not exist without you, and we do not take the responsibility of safeguarding your capital lightly.

Second, as you know, we have been investing in the business to improve performance whilst also controlling costs. 2025 marked the first full year of operation of our new funds (GQE & Knebworth), which allow us to reduce any tax you pay and better deploy our quantitative-based strategies.

This year, with the merger of Rayliant’s ETF business, we will deploy our new portfolio management model. This is the result of Justin’s work in fusing current industry techniques with his own proprietary research into Bayesian probability. Justin – in his capacity as Dr Hayward – recently gave a paper on it at the famous Max Planck Institute in Hamburg. He also has a book coming out shortly.

“A man’s got to recognise his limitations.”

—Magnum Force

Finally, we are asked more about UK politics, so we decided to bring in outside experts to help us navigate the increasingly fraught geopolitical world. So, Helen Thomas of BlondeMoney has kindly written a section for us on the geopolitical events likely to shape this year, and has also recorded a podcast.

I first worked with Helen’s company when I was at JPMorgan, and she was one of our external advisors. Helen is a former financial markets trader, and her business is not only about identifying geopolitical risks but also applying hard probability-weighted outcomes. She has written a bumper section on her year-ahead outlook.

Despite the gains, we’ll trim selectively into strength. Our long experience in the markets has taught us that while gold mining companies can be a good investment, they can also be highly volatile.

“It’s a question of methods. Everybody wants results, but nobody wants to do what they have to do to get them done.”

—Sudden Impact

2025 Review

Overall, despite most portfolios comfortably beating their benchmarks, we are slightly frustrated with our performance in 2025. It was a peculiar year.

As quantitative-based fund managers, we are driven by the maths of probability. So, we know better than most that just because something is more probable, it doesn’t make it a certainty. Sometimes you have to wait long enough for favourable odds to play out. This was the second half of 2025 for us.

Let me explain.

What Worked

H1’2025 went as we expected, with the new Trump regime behaving as cavalier as expected. This caught the market by surprise, and we took advantage of the disruption surrounding his tariff ‘liberation day’ to deploy capital.

We also rightly guessed that the new Trump administration was no more serious about fixing the US government’s spending than the Biden administration was. So, our investments in gold paid off.

Our investments in Asia also did well as China is trying to stimulate its rapidly deflating economy. We don’t think this will ultimately be successful, and China’s deepening problems are likely to trigger wider macro and political problems over the coming years, but that is a discussion for another time. In the short run, our positioning paid off.

We also exited much of the defence stocks at premium valuations as reality dawned that the EU doesn’t have the money to rearm at any meaningful level.

“Nothing wrong with shooting, as long as the

right people get shot.

“

—Magnum Force

What Didn’t Work

The first issue was our old friend probability. As we previously mentioned, the US had to extract a vast amount of liquidity from the market in Q4.

Usually, this leaves the market in a fragile state and prone to corrections. Timing these things is extremely hard, so we decided to run a higher cash balance as a result. It was prudent. However, whilst ice cracked, so to speak, it didn’t break as it had in March, so while it protected your capital, it did cause us some relative underperformance. We didn’t lose money, we just didn’t make any during this time.

Vix Aka ‘ The Fear Index’ Whilst The Market Did Wobble – As We Expected – It Never Reached April’s Levels. The Ice Cracked but Didn’t Break.

Source: Bloomberg, November 1, 2025.

Our models still see weakness in asset markets for a variety of reasons, with the next period of weakness or ‘thin ice’ likely to emerge from late February onwards.

But the main drag on performance was the strong performance of GBP across the year. The currency rallied throughout the year despite a constant stream of deteriorating economic data and political ineptitude.

As You Can See the Pound Weakens When the Market Gets ‘Scared’, but Over the Year It Rallied

Source: Bloomberg, November 1, 2025.

Longer Term GBP Weakens Against the USD

Source: Bloomberg, November 1, 2025.

Against the Swiss Franc, It Is Even More Catastrophic

Source: Bloomberg, November 1, 2025.

Since we are globally diversified FX can produce a drag in the short term.

Why is this? The first is, using the standard of metrics of FX, on a SPOT basis (ie today, all things being equal), GBPUSD is ‘fair value’ around 1.33-1.35. At the beginning of the year, it was undervalued. We were aware of this.

But markets are generally forward-looking, and that was the issue. First, a currency investment is two positions: what is going to happen to GBP, and what is the currency you are referencing against? Positioning has shown that for most of the year, investors were strongly betting against GBP, when the data turned out bad, BUT not as bad as expected, it caused a squeeze. The second part is in the case of the USD; investors were very bullish on the USD, too bullish in view of the madcap financial antics of the Trump Administration, which caused more USD weakness than the market had anticipated.

Our big portfolio hedge against this was, of course, gold mining firms, which rallied. In fact, it has rallied so much that it has become a material part of some portfolios. We still think our thesis is intact, but it is a highly volatile asset and prone to both market liquidity conditions (which are tightening) AND sentiment. So, we have trimmed the position as it is likely to have a bumpy ride over the next few quarters. Be warned!

AUCO – It Had a Good Year but Gold Is Very Volatile

Source: Bloomberg, November 1, 2025.

What Could We Do Differently?

The obvious question is, why don’t we hedge FX? The first point is that research has shown FX volatility tends to wash out after a couple of years. It’s annoying, but it’s only noise if our underlying investments are correct.

The second is that FX hedging is a bet in itself; you are fixing the price at a point in time. It also adds costs and a layer of complexity to portfolio management, requiring financial engineering, such as derivatives and margining requirements. We are not opposed to this, but only if we have a good reason to. However, at times of extreme stress, such as during the Lehman default, the early stages of the COVID-19 lockdown or more recently, the LDI debacle in the UK, the hedges quickly turn into risk themselves.

Third, we like the diversity during periods of market stress; there is usually a rush to the US dollar. Since we aim to profit from these, we tend to let USD balances build up ahead of likely stress points to profit from them. It worked in March of 2025, but didn’t in Q4. We suspect it will in 2026.

The final part is that we don’t actually like GBP, but there again, neither does anybody else! As our soon-to-be ex-Prime Minister keeps warning his own MPs, replacing him is likely to cause a financial crisis. The market is indifferent to firing Starmer & Reeves; all they care about is who replaces him. Most likely candidates are viewed as worse.

Our internal estimates suggest that Sterling is currently overvalued by approximately 15% to 20% on a trade-weighted basis. Maintaining the current exchange rate would require a level of productivity growth that is not currently evident. We believe it will be difficult for Sterling to maintain this strength; eventually, gravity asserts itself.

In essence, the UK is living beyond its means. But so are other countries; the difference is that the UK has close to zero productivity growth, zero economic growth and ever-growing borrowing to fund more inactivity. None of this is likely to change with the current policy mix chosen by the government.

The US also plans to devalue its currency, but we just think it’s more likely GBP will go first. So by splitting currency up a bit, this offers some element of diversification too. The giant Wellcome Trust also runs a currency-diversified portfolio too. Or as they put it ‘Don’t put all your eggs in one currency’.

The View from the States: Consensus vs. Reality

Looking forward to the coming year, specifically regarding the all-important US market, we must start with a humble admission: in the short term, we do not have any particularly strong directional views. The market is a complex adaptive system, and short-term noise often drowns out the signal.

Instead, let us examine the consensus, which is undeniably bullish. The prevailing narrative is that everything in the United States is proceeding perfectly: tax cuts are flowing through, interest rate cuts are lowering the cost of capital, and the economy is being aggressively stimulated by a government led by a President who, as we know, will do essentially whatever it takes to win the midterms.

However, history offers a cautionary counterpoint. Mid-presidential cycle years tend to be notoriously weak for equity markets.

Additionally, if one looks below the glossy surface of the headline GDP figures, the US economy is beginning to show significant divergence. While a select few are doing very well out of this regime, an increasing number of Americans are struggling with persistent cost-of-living problems. There is a very high probability that, just as inflation and economic dissatisfaction caught up with the Biden administration, these same forces will catch up with President Trump at the ballot box.

Furthermore, there is a dangerous assumption embedded in current market pricing: that the US can continue to borrow indefinitely without consequence. That remains to be seen. The bond vigilantes have been quiet, but they are rarely silent forever.

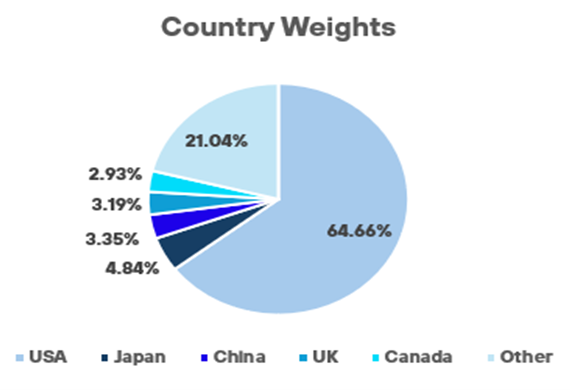

The Crowded Trade: Do You Know What You Own?

This brings us to the most significant risk in modern portfolios: the illusion of diversification.

If you look at the average private investor’s portfolio today, or indeed many professional discretionary managers, you will find a startling uniformity. Through the proliferation of passive index funds and US-centric global equity mandates, almost everybody has huge exposures to the same handful of US technology firms.

Because these companies have grown so large, they now dominate the indices. Owning the “market” no longer means owning a slice of the global economy; it means making a concentrated bet on US Big Tech.

Most investors are deeply overweight US stocks and technology stocks in particular, often without realising the extent of that concentration. When the tide turns in that specific sector, there will be nowhere to hide for those who merely “bought the index.” We prefer to know exactly what we own, and more importantly, what we are paying for it.

Most Diversified Portfolios Are Very Biased to the US

Source: MSCI.

Knebworth: The Invisible Yield

This was the first full year of operation for Knebworth. While the headline number may appear softer than the underlying reality, we are satisfied with the fund’s structural health.

The portfolio is performing exactly as designed—mimicking the high grade safety strategies used by JPMorgan’s Chief Investment Office and remaining defensive while waiting for market stress to deploy capital into new assets. The reported yield is being temporarily understated due to currency translation effects: the fund holds a deliberate pool of US Dollars intended for deployment during periods of market dislocation, and the recent strength of Sterling has reduced the GBP reported value of these holdings.

The Takeaway: Yield generation has met our expectations. The gap between the “reported” number and the “real” return is largely optical and reflects temporary currency movements. As exchange rates normalise, this gap should narrow.

Despite Rate Cuts and Our Caution, Knebworth’s Underlying Yield Met Expectations

Source: LGT (our fund administrator).

Conviction over Consensus

As we enter 2026, the easy choice would be to chase the consensus into an overcrowded US technology sector; many know it’s a risk, but the hope is for one more good year. Many of our competitors have no choice; they are too big to realistically diversify anyway.

However, just because a trade is probable does not make it a certainty, and we prefer to know exactly what we own.

Our data suggests the UK is living beyond its means and that Sterling’s gravity-defying rally cannot hold. Will it be this year? We don’t know, we just believe over time it will. When this anomaly corrects, the “coiled spring” within our strategy will release. Until then, we will not abandon high-quality assets for the sake of short-term optical comfort.

We appreciate your continued partnership and your willingness to look past the noise. The herd is feeling lucky; we prefer to be prepared.

Thank you for your continued trust. And with that I will hand over to Helen!

—Ben Ashby

![]()

Thank you to all at Henderson Rowe for the opportunity to provide my humble contribution to your quarterly outlook. My business, BlondeMoney, analyses the unpriced risk in financial markets. This is often, but not always, political risk. We strive to provide unique insight into the worlds of Westminster and the City. I’ve had a foot in both, having been an adviser to George Osborne during the banking crisis as well as working for investment banks and as a fund manager. Prior to this, I graduated from Christ Church, Oxford with an MA in Politics, Philosophy and Economics. I’m a Fellow of CFA UK and Freeman of the City of London.

Politics and Risks in 2026

Keir Starmer’s premiership is already over in all but name; Westminster is merely waiting for the excuse to say so out loud. Within the Labour Party, this reality has hardened into something approaching panic, with the search for a trigger event, the proverbial last straw, already under way. Waiting until after the May elections would be a strategic error. By then, the damage to Labour’s authority and internal discipline may be irreversible. A low‑grade cold war inside the party, long tolerated in the hope of stability, has reached the point where it must be resolved quickly and decisively. Otherwise, the greater fear for Labour – that they might not only be thoroughly beaten but potentially eradicated by a thumping Farage‑led government – will become ever more likely.The year begins with the once‑confident Labour government perched precariously, confidence indicators sagging, backbench restiveness growing, and a leadership transition likely before the summer. The configuration of that transition, and the signal it sends to markets and global partners, will shape investor sentiment and fiscal forecasts well beyond Britain’s shores.

- Starmer’s Waning Authority: Why the End is Near

For much of his time as leader of the Labour Party, Sir Keir Starmer was positioned as the antithesis of the tumult that characterised Conservative governments of the prior fourteen years. He promised stability, competence, and discipline. The self-proclaimed son of a toolmaker and former Director of Public Prosecutions would be a rather dull but capable managerial leader for uncertain times. Instead, the narrative has shifted.

From freebies to u-turns, from broken manifesto pledges to leaky tortuous budgets, Keir Starmer has presided over the most precipitous decline in support for a government in modern times. The latest polls put the Labour Party in third place, having lost half of its vote share since the general election at which it won a landslide majority. Haemorrhaging supporters to both its left and right flanks is proving an insurmountable political challenge for a man who even tacitly admits the job is beyond him. At his latest appearance in front of parliament’s powerful Liaison Committee he acknowledged “my experience now as Prime Minister is of frustration”. He mimed pulling a lever as he complained how “the action from pulling the lever to delivery is longer than I think it ought to be”. He said almost exactly the same a year earlier, suggesting more time in the role is not yielding better results.

And yet we start a new year with the same occupants in Downing Street. This has led to the lazy assumption that a Labour leader cannot be displaced because incumbency is inherently stabilising. This is incorrect. The Labour Party has every procedural means to force a leadership contest, and on the basis of recent leadership and deputy leadership elections, the process could be completed within six to eight weeks.

Labour’s internal rules were amended in 2025 to allow leadership challenges at any time rather than only at annual conference, dissolving what was once a significant barrier to change. The hurdle that 20 per cent of MPs must back a challenger is not especially onerous, as evidenced by the 316 MPs who quickly declared their public support in last autumn’s deputy leadership contest. That took place in the wake of the sudden departure of Angela Rayner. She resigned on 5th September 2025 and within a week MPs had made public their nominations for their choice of replacement deputy leader. Six weeks later, the results were announced. The machinery of change is now in place.

Some of the reticence to start the process comes from the fact that the rulebook states “The sitting Leader shall not be required to seek nominations in the event of a challenge”, meaning Starmer can remain on the ballot. This is what provoked the message from Downing Street sources last November that “allies of the prime minister are making it clear he would fight any challenge”. In other words, moving against the PM would not necessarily take him out in a clean strike, as Labour members might keep him in post by voting for him in the eventual ballot. This would be a pyrrhic victory, as former prime ministers can attest. Once you crystallise the quantum of your opponents, your authority is weakened beyond repair. Margaret Thatcher won the first round of the leadership contest that ultimately saw her out of office nine days later.

There are also weapons available in the process that exist beyond the rule book. In 2016, Labour MPs voted overwhelmingly 172 to 40 that they had no confidence in their leader, Jeremy Corbyn. Corbyn simply responded that that ballot had no “constitutional legitimacy” as it was in no way binding upon him. He ploughed on into the following year’s snap election. Those years were bruising for many Labour MPs and Labour Party members, reinforcing the sense that Starmer might be able to survive. But there is one key difference in the current environment: the leader of the Labour Party is also the prime minister. Machinations against Corbyn were largely irrelevant as he was simply leader of an incoherent opposition. It’s simply not sustainable for the head of the government to continue in post when less than one-fifth of voters support his party and his working majority in parliament has all but evaporated.

This is uncharted territory for Labour. Since its founding at the turn of the 20th century, the party has governed for barely a quarter of that time. As a result, there has been only one previous instance of a leadership contest occurring while the party’s leader was prime minister. That came in 1976, when Harold Wilson’s sudden resignation triggered a scramble among four MPs, with James Callaghan ultimately emerging victorious.

Starmer’s predicament is not solely procedural but reputational. His net favourability rating has sunk to levels comparable to Boris Johnson’s on the day he resigned, and as low as Jeremy Corbyn’s at his nadir. In practical terms, this suggests a leader who has not only lost momentum but credibility.

Waiting for the results of elections in Scotland, Wales, and local councils to confirm what is already apparent risks far more than the simple loss of representatives for Labour. The party’s internal in-fighting now threatens to deliver the outcome it fears most: effectively handing the next general election to Nigel Farage. The ongoing divisions are eroding the very fabric of Labour, while Reform UK gains strength, scale, and momentum.

Reform has already received the largest single donation from a living donor in British political history. Any success in May — even modest — will translate into more “ground troops” in the form of elected councillors and local representatives, further professionalising the party. Nigel Farage clearly recognises the stakes, hence his exhortation to spend all the money they have as “it’s double or quits… we are just going to go for it… It is the single most important event between now and the general election“.

- The Politics of Momentum and Market Sensitivities

Political stability is a core determinant of investor confidence, currency valuations, and gilt yields. In the immediate aftermath of the Autumn 2025 budget, markets displayed signs of discomfort when u‑turns and mixed signals from Downing Street appeared to unsettle fiscal expectations.

However, despite these missteps, markets have been remarkably forgiving, buoyed by recent Bank of England rate cuts and a sense that broader global risk appetite outweighs UK domestic political fragility. This forgiveness should not be taken for granted. Continued political drift, especially if the new leadership is unclear on fiscal intent, could lead to widening spreads on UK sovereign debt, a weaker sterling, and reduced foreign investment at precisely the moment Britain needs to demonstrate economic credibility.

For markets, the arrival of a new prime minister and chancellor early in 2026 is a key event risk. Firms and institutional investors will watch closely not just the identities of those office holders, but their fiscal philosophy. A cautious, pro‑market pairing could re‑establish confidence; a more left‑tilting combination could unsettle fixed‑income and equity markets. This is why inside Westminster, speculation over names such as Wes Streeting, Angela Rayner and Lucy Powell is underpinned by even more intense focus on who will sit at the Treasury Dispatch Box.

- Who’s Next? Leadership Contenders and Market Implications

The leadership race would likely feature two familiar figures and one less well-known alternative:

- Wes Streeting, the Health Secretary, seen as a modernising centre‑left candidate with appeal to business‑oriented voters.

- Angela Rayner, a figure with strong grassroots and union support appeals to Labour’s entire left wing, from hard to soft.

- Lucy Powell, a long term party loyalist and wildcard who, by virtue of her deputy leadership position, may play kingmaker or even emerge as a compromise candidate.

Ed Miliband’s economic experience, particularly in energy and climate portfolios, makes him a name that floats in the background. But he knows that he is discredited after the electoral defeat suffered under his leadership in 2015 and another role will be of greater interest to him.

It is the choice of Chancellor that matters for markets. It is widely assumed that Labour would avoid appointing someone perceived as radically left, such as a figure overtly aligned with big spending or radical redistribution, because bond markets are especially sensitive to fiscal uncertainty. Instead, names associated with fiscal prudence and tempered rhetoric, such as Yvette Cooper or Pat McFadden, are increasingly mentioned as stabilising picks who could calm expectations and reassure both markets and international partners.

This is the central political risk for Q1: a leadership transition that simultaneously offers opportunity and anxiety. If the incoming team delivers a message of competent stewardship, it could arrest Labour’s slide in opinion polls and reset investor confidence. But if the process accentuates ideological rifts or leads to ambiguous policy signals, the opposite could occur.

- Electoral Pressures: The Rise of Reform UK and the Farage Effect

Underlying these internal party questions is a broader electoral reconfiguration. Reform UK, led by Nigel Farage, has been a disruptive force in recent local elections, snatching seats from both major parties and demonstrating that traditional two‑party dominance is no longer guaranteed. Farage’s party has professionalised its infrastructure, attracted significant funding, and positioned itself as the primary alternative to mainstream politics – a dynamic Labour strategists long feared.

The psychological impact of this shift cannot be overstated. For decades, UK politics operated under a duopoly that implicitly disadvantaged insurgent parties. While the Conservatives’ collapse in parts of 2025’s local polls was a major story, Reform’s surge has been even more consequential because it directly threatens Labour’s core constituencies as well as those disillusioned with the Conservatives.

Farage is already a PM-in-waiting. His tweets in response to the US arrest of Venezuelan President Maduro were viewed by almost 7 times more than that by the official leader of the opposition, Kemi Badenoch. The EU is reportedly demanding what EU diplomats are calling a “Farage clause” be written into closer alignment on agricultural trade, in case a future government unpicks the agreement.

This backdrop explains why some within Labour argue that the risk of a Farage‑led government is not hypothetical but imminent. There is genuine fear that if Labour clings to an unpopular leader or fails to articulate a coherent vision for governing, Reform’s momentum could translate into a seismic upset at the next general election. It is this prospect that will provide the ultimate kick required to deliver a change of prime minister.

- Policy Drift and Governance Challenges

Starmer’s government has struggled to maintain a coherent message across a wide range of policy areas, and this has exacerbated perceptions of indecision. From welfare reform rebellions to partial reversals on tax measures and complex debates over jury trial reforms, the administration has often appeared reactive rather than strategic.

In some cases, backbench dissent has grown to the point of public embarrassment, with dozens of Labour MPs willing to oppose or abstain on key votes. This level of internal fractiousness should be rare for a government with a substantial parliamentary majority. Instead it is becoming commonplace that as soon as a rowdy backbencher goes public with their outrage, a backtrack by Starmer and Reeves promptly follows. It’s almost unheard of for the government to issue any fresh directions ahead of the Christmas break but on the day before Christmas Eve, the country was suddenly informed of a partial reversal of the so-called family farms tax, by increasing the threshold for inheritance tax relief. The National Farmers Union President welcomed the u-turn, pointing out ‘We have had hours of calls with Labour backbenchers, particularly those representing rural seats, resulting in a rebellion with nearly 40 abstentions on the vote on Budget Resolution 50”. One Labour MP, Markus Campbell-Savours, had the whip removed for voting against it. He represents one of the most rural seats in the country and his father is a Labour member of the House of Lords, having been a Labour MP for twenty-two years in a neighbouring constituency. This hardly makes Campbell-Savours a known troublemaker.

Losing such an MP ahead of the passage of the rest of the Finance Bill does not bode well.

This is not merely a tactical problem but represents a deeper issue of party unity and discipline at a time when government credibility is under scrutiny. For markets and business leaders, policy clarity and predictability are essential. Uncertainty, particularly when it emanates from internal party dynamics rather than opposition ambushes, creates risk premia that can depress investment and stall hiring decisions.

- The Political Calendar and Forward Expectations

Looking ahead to Q1 2026, several dates and events merit close watching:

- Starmer trip to China – the Prime Minister is due to make his first bilateral visit to China at the end of January

- Finance Bill legislation – proceedings in the Public Bill Committee must conclude by 26 February 2026

- The Spring Forecast – now a forecast rather than a statement, the OBR will not judge whether the Chancellor is meeting her fiscal rules but instead simply provide an update on the economy on 3 March 2026

Through all of this, keep an eye on the polls, particularly those with data on the upcoming May elections to the devolved assemblies in Wales and Scotland. Both have been Labour heartlands and losing support to nationalists in both regions would be deeply unsettling for the Labour Party to stomach.

- Conclusion: Stability Through Change or Prolonged Drift?

The first quarter of 2026 will test the resilience of Britain’s political institutions and the adaptability of its economic framework. The near‑inevitable end of the Starmer premiership opens a window of opportunity for Labour to reset, unify, and articulate a clear economic agenda. But it also presents a moment of heightened uncertainty that markets and business leaders cannot afford to ignore. Ambiguity and division risk exacerbating a lean growth environment and elevating risk premiums on UK assets.

For investors and corporate boards, the key signals will come not just from political pronouncements but from the credibility and coherence of economic policy that emerges alongside any leadership transition. A team that emphasizes fiscal responsibility, clarity of purpose, and strategic direction could stabilise both markets and public sentiment. Despite winning a huge majority, the government has been dogged by a lack of mandate. “Change” from the Conservative Party does not necessarily translate into removing benefits from pensioners and the disabled, taxing jobs and harming family farms. If anything, it looks to many voters like more of the same. A new Labour leader, by contrast, could present a coherent policy platform that not only shores up the party’s support but also prevents it from facing existential decline on the national stage.

Ultimately, the political and economic fate of Britain in 2026 will hinge on whether the post‑Starmer Labour Party manages to transform internal turmoil into constructive renewal – or instead spirals into disunity at precisely the moment when firm leadership is most needed.

—Helen Thomas

Important Information

This document is issued by Henderson Rowe for information purposes only. It does not constitute a personal recommendation, investment advice or an offer to transact. Past performance is not a reliable indicator of future results and the value of investments can fall as well as rise; you may not get back the amount you invest. Any views expressed are subject to change and may become outdated. Investments may not be suitable for every investor and you should seek advice based on your individual circumstances.