Dig out your flares, tuck into some Angel Delight, and listen to the Bay City Rollers. The 1970s are back!

Talking Points

- The damage to the energy infrastructure in the Gulf is real, and so is the real-world impact

- There is, in all probability, a huge shock coming to the economy

- Fortunately, we expected something like this and have prepared for it. But we warn it will be bumpy

- This is the first external shock the current government has experienced. It is likely to trigger greater dysfunction

“Well. Here We Are Again” – The Statler Brothers

Those of you who have been clients for a while will know we have been banging on about the return of the worst elements of the 1970s for some time now. The song title above captures the situation better than we could.

We have also been pointing out – in client notes, in podcasts, in the occasional exasperated paragraph on this very platform – that the UK had neglected the importance of energy security or indeed energy’s role in an advanced economy. Plus, Israel and Iran had, shall we say, unfinished business. The 2023–2025 period of “managed tension” always looked to us like an intermission rather than a finale. It was.

The Strait of Hormuz is now functionally closed. Ras Laffan – the world’s largest LNG facility – has taken serious damage. QatarEnergy has declared force majeure. In late March, the IMF, not usually given to drama, said the UK is facing one of the largest economic shocks of any country from the Middle East conflict, and is “especially exposed” to surging energy prices due to its heavy reliance on gas-fired power. The Prime Minister urged the public to “act as normal.” We’ll leave that one there.

Despite Being a Bigger Crisis, Oil Prices Remain Below the Levels Seen In the Ukraine War

Source: Bloomberg, April 13, 2026.

First, a brief history lesson: the economic shocks of the 1970s were triggered by excessive money printing in the late 1960s and early 1970s. In the US, it was to finance the Vietnam War and LBJ’s Great Society, and in the UK, it was Heath’s Dash for Growth. This laid the groundwork for when the Yom Kippur War triggered the OPEC oil embargo and the first oil price shock.

The economic disruption, along with the rise in inflation that drove higher rates, created a negative feedback loop across the economy and led to further problems, including a major banking crisis that nearly brought down NatWest. It also exposed the rot in the system. There is a narrative that the Thatcher reforms of the 1980s decimated British industry. But what is not adequately explained is that many of those firms were already ‘zombie’ companies propped up by the government, and the government could no longer afford to do so at higher rates. The restructuring actually started after the 1976 IMF bailout. It marked the effective end of the post-war economic model and triggered significant political instability as the regime shift started.

This is likely to prove similar for this era. The key difference is whilst the restructuring was in corporate balance sheets this time it’s likely to be excessive welfarism and the size of the state that are likely to undergo similar restructuring over the coming years. The current path is unsustainable and it’s a poor use of resources. On a macro level, the gigantic trade deficit shows the UK is over consuming relative to what it produces and needs to sell things or borrow to make up the difference. This isn’t a political comment, just an economic reality. Like the 1970s, we suspect the market is going to force these tough choices upon the government.

Unfortunately, as Helen Thomas discusses in her section, this government hasn’t yet faced a true external shock and appears wedded to this current status quo. Which makes its (almost record) unpopularity even more ominous.

Therefore, we caution that the UK headlines are likely to worsen. Nor can we predict how this government will react. Do they take the necessary painful decisions or double down to shore up their ‘core vote’? As shown below, the Chancellor’s social media feed appears to be championing more welfarism and regulation. The economic incoherence over the past two years may increase and further damage investment opportunities.

The Chancellor’s Recent Social Media Conspicuously Doesn’t Mention Anything Positive for Taxpayers or Businesses. Remarkable.

Source: X, April 6, 2026.

We are on the cusp of an enormous economic shock across the UK and large chunks of the global economy. In some ways, it’s similar to the 1970s, but in other key ways, it’s worse.

“Let’s go to the Winchester, have a nice cold pint, and wait for this all to blow over.”

— Shaun of the Dead

Here’s the critical difference from 1973 that most commentary misses: The Arab oil embargo was a political act, meaning it could be reversed politically. OPEC opened the tap; OPEC could close it. This one has a different character entirely.

There is also the small matter of physical infrastructure. Ras Laffan is not a software bug that gets patched overnight. And energy import dependency has increased as domestic oil and gas production has declined, leaving the UK more vulnerable to gas supply shocks. A hole the current government has spent the last two years enthusiastically making larger. The timing is, as they say, suboptimal.

The damage in the Gulf is real. There seems to be no obvious way to resolve this war. It seems unlikely that there will be a political change in Iran toward a more peaceful regime and a ‘normalisation’ in the region, which is the only ‘good’ economic outcome. It is quite possible that Iran will become the new Libya and disintegrate into a fractional or failed state. Or it might be that we have created the new “North Korea” with an even more oppressive state prone to firing missiles and making nuclear threats whenever it doesn’t get its own way.

Currently, the market isn’t priced for this and appears to think that Trump will walk away and it’s back to business as usual.

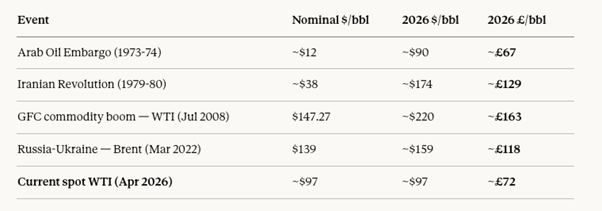

Nor is energy yet expensive. If we adjusted the previous spike for inflation, the spot price would be $220 dollars per barrel. Oh, and GBP had more purchasing power then. So, we may see prices double from here.

Source: Henderson Rowe Research, April 13, 2026.

But there will be differences. As the collapse of Credit Suisse showed, we live in a digital age and events seem to unfold far faster than previously. Additionally, we have a faltering bubble in AI investments, with data centres being very heavy energy users, and energy is about to get expensive. Finally, we have a US administration that makes Nixon’s ‘Mad man’ strategy of the 1970s look positively dull.

“We had joy, we had fun, we had seasons in the sun.”

— Terry Jacks

What does this mean for you?

Financial commentary loves to discuss energy shocks in terms of basis points and GDP deflators. Let’s be more direct.

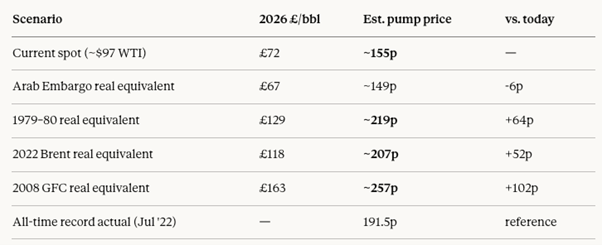

The petrol station is where people will feel it first—prices are already moving and the direction is not ambiguous. If Hormuz stays closed at any meaningful level, the trajectory is higher. We’re not forecasting 1970s-style queues around the block, but we wouldn’t rule out a degree of panic buying if the headlines get sufficiently alarming. It only takes the belief that there might be a shortage, not an actual shortage.

Time To Buy A Tesla?

Source: Henderson Rowe Research, April 13, 2026.

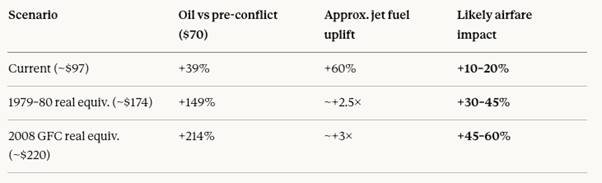

But the garage is the visible part. The less visible part is that energy is an input into essentially everything. Food prices—already doing their own thing—will rise further, because modern agriculture runs on diesel and fertiliser. Flights are getting more expensive; airlines are already repricing. Every energy-intensive manufacturing process in the country faces higher input costs. The Bank of England has to choose between raising rates in a weakening economy and letting inflation expectations drift. There is no good option on that menu, and they know it.

Time To Book that Airbnb in Clacton?

Source: Henderson Rowe Research, April 13, 2026.

And—this is the bit we really want clients to internalise—we think we are near the beginning of this, not the end. Markets are still, in aggregate, pricing a fairly tidy resolution. We disagree.

What We’ve Done About It

The short version: we saw this coming, we positioned for it, and the portfolio reflects that.

A Word on Currencies (Or: Why Your Portfolio May Look Odd For a Bit)

Our bias—and we acknowledge this runs counter to the current consensus—is that the dollar strengthens from here. The reasoning is straightforward. The dollar almost always benefits from a flight to safety, and whatever else this is, it’s a flight-to-safety environment. Beyond that, financial conditions are tightening worldwide as volatility increases, which historically pulls capital toward dollars. And there’s a less-discussed dynamic we think matters: the Gulf sovereign wealth funds—some of the largest pools of capital on earth—will need dollars. Not for investments. For imports. Countries that have suddenly stopped exporting oil and gas still need to buy food, medicine, and rather more besides. They will be liquidating assets to fund that, and the currency they need on the other side of those trades is USD.

So Far the USD Has Been Strengthening

Source: Bloomberg, April 13, 2026.

That said, predicting GBP/USD specifically is harder than it looks right now, because the UK is running a relatively tighter fiscal policy than the United States, which provides some support to sterling that partially offsets the dollar’s safe-haven pull. The short version: we expect USD strength broadly, but the GBP leg of that trade has more moving parts than usual.

We are not going to pretend we can confidently call the precise path of this. Nobody can. What we can say is that we are comfortable with our FX exposure given our medium-term view, and we’d encourage clients not to read too much into short-term swings in the currency line of their statements.

Don’t Panic

We’re going to be honest: it will probably get bumpier before it gets better. As the market gradually realises that this isn’t a temporary disruption to be waited out, there will be volatility. Some of it will be unpleasant. This is the nature of the thing.

But here is the other side of that coin. The superior long-term return from equities exists precisely because investors need to be compensated for exactly these periods—and you only really benefit from it by being prepared to weather the occasional storms. Unfortunately, many investors fail to stay the course and, overcome by financial seasickness, often tend to panic at the height of the storm and leave. The investors who were buying in the autumn of 1974, when every front page was catastrophic, and the consensus was despair, made extraordinary returns. The ones who waited on the shore for calmer seas missed the best of it.

We are actively working on the list of things we want to own as this repricing creates its opportunities. There will be genuinely excellent buying opportunities ahead. We intend to take advantage of it.

More soon. And now I’ll hand over to Helen.

– Ben Ashby

Note: All data correct as of April 13, 2026.

![]()

Geopolitics, Scarcity, and the Limits of Policy

“It’s much more important that this be successfully completed than what the market does.”

— Jamie Dimon on the Iran conflict.

For much of the past decade, markets have operated under the comfortable assumption that politics might create volatility, but policy would ultimately stabilise outcomes. Central banks could ease, governments could spend, and supply would respond.

That assumption is now being severely tested.

What we are witnessing is not simply another cyclical shock, but the intersection of geopolitical conflict, physical scarcity, and constrained policy frameworks. We are in a supply shortage that no protagonist can solve and that the belligerents are incentivised to maintain, if not exacerbate. Stimulative monetary and fiscal intervention is not only useless but counterproductive in such a stagflationary shock, even as electorates will demand action. Bond markets and voters are set for an explosive showdown as governments with weak mandates inevitably fail to please either.

Inflation: From Transitory to Structural

The immediate consequence is renewed upward pressure on inflation. Expectations are shifting again, with recent surveys in both the UK and US showing a marked increase in short-term expectations. Central banks can tolerate temporary spikes; they cannot tolerate a de-anchoring of expectations.

What is becoming increasingly clear is that the disinflationary environment of the past two decades was not structural, but contingent—reliant on abundant global supply, efficient trade flows, and a broadly cooperative geopolitical backdrop. A 2–4% inflation range now appears more plausible than the 0–2% target bands that defined the post-financial crisis era.

Bond Markets: The Real Constraint

In a traditional slowdown, weaker growth would support government bonds. That relationship is now under strain. Governments are entering this period with elevated debt levels, persistent deficits, and limited room for manoeuvre. If investors begin to question fiscal sustainability, yields can rise even in the face of weakening growth.

For the UK, this constraint is particularly binding. The DMO forecasts £252bn of gilt sales this year—almost half as much again as the £170bn issued in the Truss/Hunt 2022-23 fiscal year—while political resistance to spending restraint limits the scope for consolidation. The result is a narrowing policy corridor: too little intervention risks political backlash; too much risks market destabilisation.

Geopolitics: The Underlying Driver

The disruption centred on the Strait of Hormuz is not simply a logistical problem; it is a manifestation of a broader contest over the future structure of the global economy. Iran retains a uniquely asymmetric position — the geography of the Strait provides a relatively low-cost mechanism to exert global economic pressure, and the incentive to maintain disruption rather than resolve it is clear.

On the other side, the United States has articulated an increasingly explicit strategy of economic segmentation. Writing in The Economist, Treasury Secretary Scott Bessent concluded that a more segmented system would provide stronger tools to address global imbalances, and that the cost of remaining outside a US-led economic bloc would be high. This is not the language of globalisation. It is the language of economic realignment. Within that framework, disruption is not necessarily a failure. It can be a feature.

Even in the event of de-escalation, the implications will persist. This is not a shock that can simply be unwound.

The UK: Policy Meets Constraint

It is in this context that the UK’s position appears particularly fragile.

Keir Starmer’s leadership has been defined by caution, legalism, and a preference for process over politics—traits effective in opposition but less well suited to a period that demands decisiveness and political authority. That authority has been severely eroded. The loss of Morgan McSweeney, who helped deliver the party’s landslide victory, has further reduced central control.

Not only losing but coming third in the Gorton & Denton by-election has left the Labour Party in an existential crisis. The Green victor’s words will only ring more true as the stagflation picture permeates through the electorate: “Working hard used to get you something. It got you a house, a nice life, holidays. But now—talk to anyone here and they will tell you, the people work hard but can’t put food on the table, can’t put their heating on, can’t even begin to dream about ever having a holiday.”

Meanwhile, the balance of power within the party is shifting. Ed Miliband has re-emerged as a central actor, with reports of his opposition to US military action and growing visibility in policy debates suggesting he is operating as a de facto leader following a bloodless internal coup. The prospect of a reshuffle elevating him to Chancellor would formalise this shift. His framework—state intervention, energy transition, redistribution—sits uneasily alongside the fiscal constraints outlined above.

This tension is already visible. Last year’s welfare reforms—not even cuts, merely slower growth in spending—had to be gutted at the despatch box, with 47 Labour MPs still voting against. If another 33 baulk at future consolidation attempts, the government will have lost its working majority.

Conclusion

The UK is entering a period in which the traditional assumptions underpinning asset allocation—stable inflation, predictable policy, clear institutional authority—can no longer be taken for granted. Gilt markets are likely to remain sensitive to fiscal developments; sterling may face similar pressures if confidence in policy direction weakens.

All of which leaves us with the battle royale ahead: Miliband vs the Market. As gilt yields ratchet higher and pressure for fiscal consolidation increases, Milibandism will double down in the opposite direction.

—Helen Thomas

Important Information

This document is issued by Henderson Rowe for information purposes only. It does not constitute a personal recommendation, investment advice or an offer to transact. Past performance is not a reliable indicator of future results and the value of investments can fall as well as rise; you may not get back the amount you invest. Any views expressed are subject to change and may become outdated. Investments may not be suitable for every investor and you should seek advice based on your individual circumstances.