Market Overview

The Fed Chair, Jerome Powell, was expected by many market commentators to be more pragmatic than his predecessors Janet Yellen and Ben Bernanke. Unlike an academic economist, Mr. Powell would brush aside short-term market gyrations and pay little attention to Wall Street’s fear of market volatility. 2019 was anticipated to be the year when for the first time since 2008 the aggregate balance sheet of the world’s major central banks would start shrinking. Mr. Powell was leading the way by delivering four rate hikes in his eleven-month tenure.

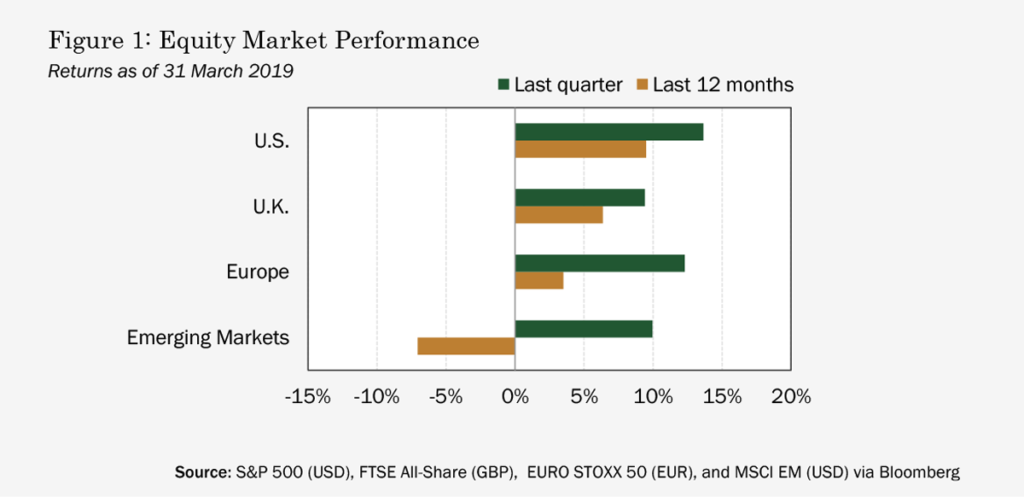

Enter the December 2018 sell-off. MSCI World lost over 13% in two weeks and the S&P 500 dropped almost 16% over the same period. Mr. Trump’s “tariff wars” have also been adding fuel to the fire. One of China’s retaliatory tariffs on the U.S. food and agriculture hit about $20.6 billion worth of US exports. A tough pill to swallow for some of Trump’s core base states.

The US economy is still one of the key drivers of the global business cycle. This is due to the direct impact of US interest rates on the global economy via financial markets. In fact, except for the Global Financial Crisis the US has been propelling the global economy through most of the last 100 years.

If this positive impact of the US demand fades will there be another economy ready or willing to pick up the baton?

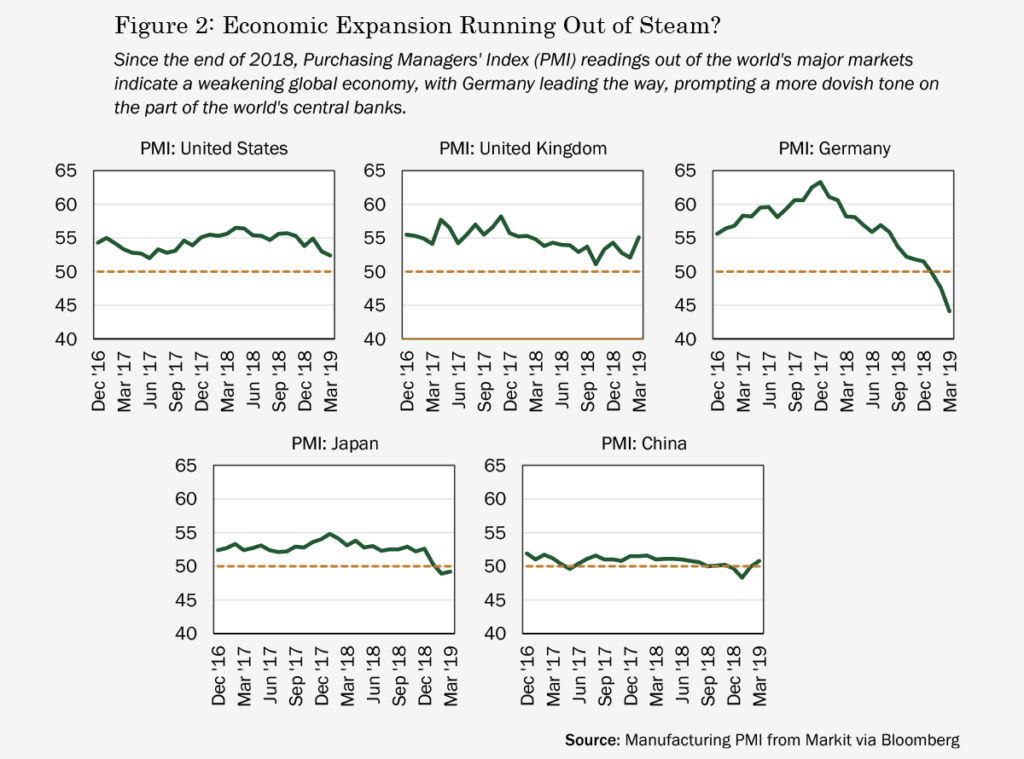

China is likely to see growth slow towards 6% with the US trade policy putting considerable strain on its economy. Also, trade tariffs are already trimming global growth through supply-chain disruption, higher uncertainty for businesses and higher import prices. The Eurozone has been one of the first victims of the US-China trade war. Germany’s March manufacturing PMI index approached a recession like reading of 44.7 from a high of 63 recorded fourteen months ago.

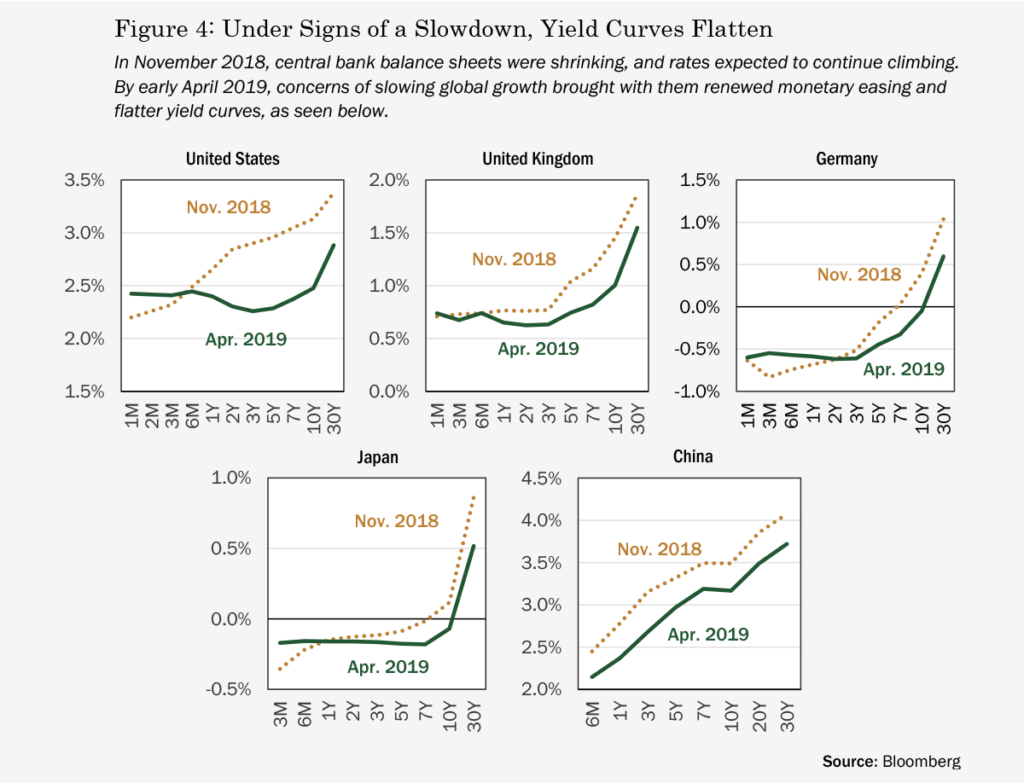

However most major central banks have already spotted trouble on the horizon and started winding down the QT rhetoric therefore realizing that the window of opportunity for monetary policy normalization has closed. The Fed went from a hawkish “Quantitative Tightening (QT) on autopilot” in June 2018 to a more dovish and patient “wait and see” approach in March 2019. Chinese policymakers decided to step in as well. Yuan-denominated bank loans rose 40% year over year in January. According to the Wall Street Journal this was the fastest singlemonth growth since records began in 1992.

European policymakers are not sitting on their hands either. During its March meeting, the ECB proposed a new series of quarterly TLTROs (Targeted longer-term refinancing operations) after it had revised next year’s Eurozone’s growth projections from 1.7% to 1.1%. With the UK government hell bound on taking its withdrawal talks to the brink, the BOE has been signaling no interest rate hikes in the near term.

The uncertainty about further economic development therefore remains an issue, but it’s a so-called “known unknown” which would imply markets have already started discounting global economic slowdown. Under this assumption the expansion of global trade could continue, albeit at a somewhat slower pace. In other words, we might be experiencing a small recession already and because most economic indicators are lagging, we will not be able to confirm it till after the fact. Since the beginning of the year most global markets have climbed their way back to 2018 highs and most developed government bond yields had retreated back to or below February 2018 levels, when Mr. Powell was appointed Chair of the Fed. Although there might not be a single economy to take over the burden of driving global demand, it looks like bond and equity markets are expecting most central banks to come to the rescue if needed.