“I’ve had a lot of worries in my life,

most of which never happened.”

—Mark Twain

Our performance in Q12024 benefited as the massive “Not money printing, honest” year-end liquidity injection by the US authorities worked its way through the system, although going to April we saw some “chop” in the portfolio as the market consolidated as usually happens after such a strong run.

Looking ahead into the upcoming summer months, our suspicion is that we will see a more complex market environment marked by higher volatility. Although this isn’t a bad thing in itself, for reasons we discuss later.

Navigating Through Uncertainty

Our reasoning behind this suspicion includes the likely ebbing of liquidity, delayed effects of rate hikes seeping through the world economy—combined with mounting loan losses for the financial system—and the loss of favourable “base effects” in the economic data.

But the main reason is the all-important US Treasury market. Whilst the US market has benefited from the massive fiscal stimulus from the government, ultimately our view is that it’s unsustainable in the longer run.

Therefore, without a fresh injection of liquidity, we expect the rise in bond yields—which we have seen to continue since the beginning of the year—to potentially “spook” the market as it did last year. It should also cause continued US dollar appreciation as the higher relative rates draws in overseas capital.

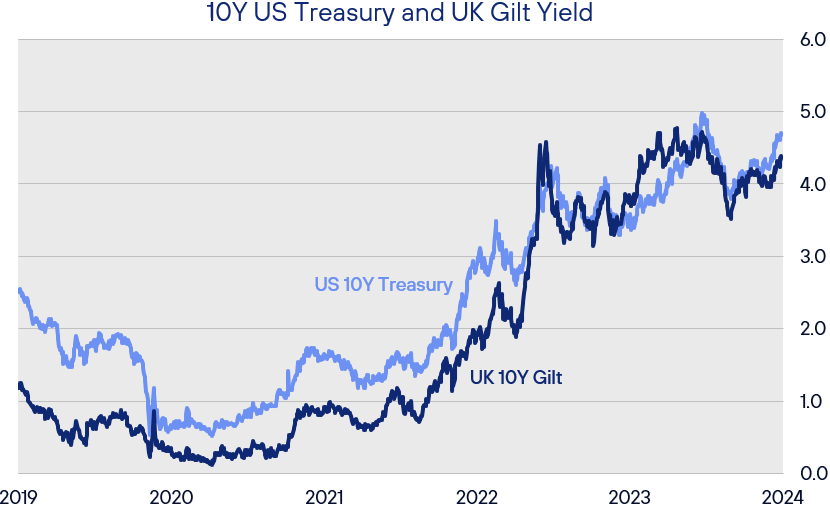

UK and US Treasury Yields Are Approaching Previous Peaks

Source: FactSet. Henderson Rowe Research.

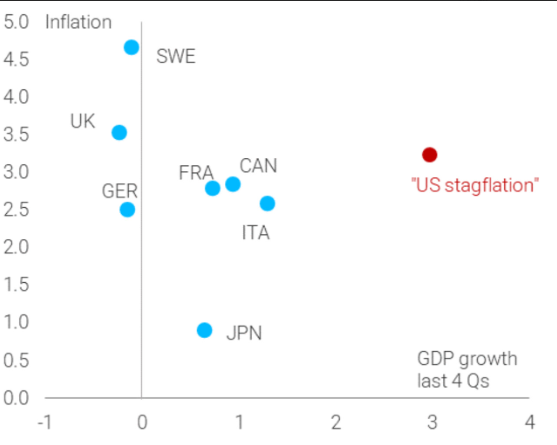

Even though we believe it’s ultimately unsustainable and the US will slip into stagflation at some point, the fact remains that currently the US economic situation remains relatively better than most of the developed world.

Whilst the US Is Likely To Falter At Some Point, It Is Starting From a Better Place Than Many Other Developed Countries

Source: TS Lombard.

“Just the facts, Ma’am” — Why We Remain Engaged in the Market

Given this forecast, a question may arise: Why do we not pull back more significantly from market exposure?

First, a suspicion is not a long-term investment strategy. It is one thing to respond to solid data and quite another to react to mere suspicions. As you know in contrast to many of our peers, we have a quantitative driven process that doesn’t allow for ego driven decisions such as hunches or suspicions by star managers.

While it is tempting to boldly reduce exposure based on potential risks, market timing is extremely difficult, and history shows investors are more likely to miss out on long-term opportunities that arise in turbulent markets than avoid losses.

It is important to remember that volatility in share prices is not the same thing as “true” risk, which is the permanent loss of capital. Equities tend to outperform bonds over time because there is more uncertainty about their future earnings. This uncertainty translates into higher volatility. Perhaps the best way to look at this is that in essence you get paid a premium for that uncertainty.

Additionally, we are mindful of the sectors and assets that appear overvalued and have taken care to minimise exposure. Our focus remains on finding value and growth in less frothy parts of the market. This approach aligns with our philosophy of risk-adjusted returns, prioritizing long-term capital appreciation over short-term gains.

Importantly, rather than tighten financial conditions, the “revealed preference” of the US authorities is to inject further liquidity when faced with problems. As we saw at the end of the last year, this can still have a powerful effect on asset prices. With a deeply divisive election due in November, we are extremely sceptical that the US authorities will allow financial conditions to materially tighten in advance of that and are more likely to inject more liquidity.

That said, we have adjusted the portfolio slightly by reducing some of the positions where we have lower conviction which raises our cash holdings accordingly. This is not a retreat, but a strategic positioning that enhances our agility, allowing us to capitalize on opportunities quickly and efficiently while also providing a buffer against the unforeseen. We expect to redeploy this cash over the coming months.

UK Politics

We are usually asked a lot about the UK. As many of you know we are good friends with Helen Thomas and the team at BlondeMoney. Helen has worked in the City as well as being a former advisor to George Osborne. Helen recently did an in-depth podcast with Bloomberg that is worth a listen.

In summary, Helen thinks that to avoid an extinction level event there is a high probability the Conservative Party will force Sunak out by July and then launch an expedited election campaign under Penny Mordaunt. They will almost certainly lose but possibly less badly than Sunak.

Labour will likely assume government, but with no great enthusiasm from the wider public by the end of summer. They will also inherit all the problems the Tories were unable to deal with. As Helen observes, the Shadow Chancellor has been floating quite left-wing policies, but with limited room to borrow and very high existing taxation levels, they seemed doomed to failure.

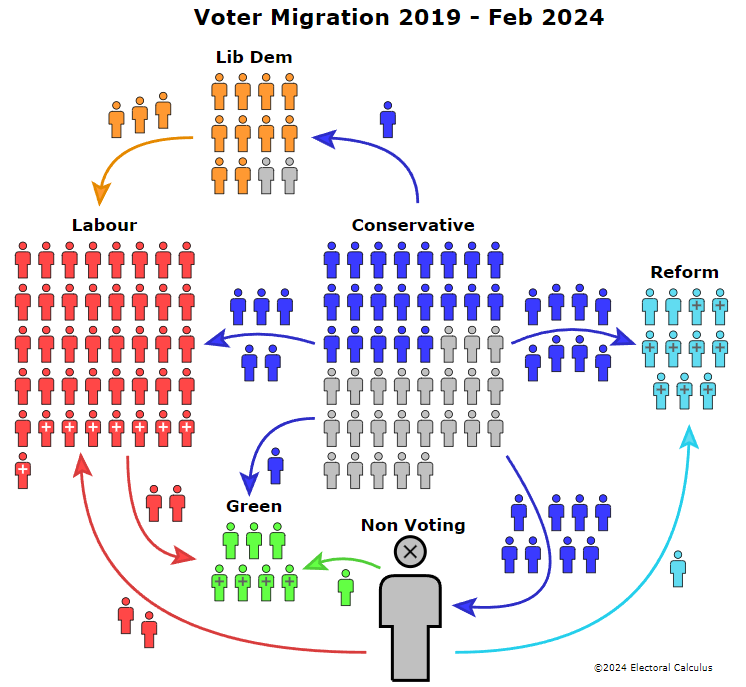

Labour’s Poll Lead Is More To Do With a Collapse of Conservative Support

Source: Electoral Calculus.

We have no strong views about Sunak’s short-term chances, but we agree with Helen that the next decade is likely to be very politically volatile and the next Labour administration is likely to flounder as badly as the current Conservative one.

Steady As She Goes

In conclusion, while the waters ahead may be choppy, our ship is well-built and our crew experienced. We are prepared for whatever the market holds and will continue to navigate towards the best outcomes for your investments.

I am, as always, available to discuss our strategy and your personal investment needs. Thank you for your continued trust and partnership.

The US economy continued surprising to the upside in Q1, with building confidence in the “soft landing” narrative and strong corporate earnings leading stocks to rally through the end of March. Against that backdrop of “risk-on” sentiment, we found ourselves—like other data-driven investors—drawn to similar positive surprises in first-quarter US inflation: a development set to derail markets’ expectations for a smooth pivot to Fed easing. Below, we highlight themes and data the team at Rayliant is following heading into Q2, along with their potential implications for the economy and markets.

Equities

The first quarter witnessed stocks around the world pick up right where they left off at the end of 2023: surging higher as investors doubled down on artificial intelligence, reacted to continuing evidence of the US economy’s strength, and clung to hopes the Fed would follow through on three cuts tipped for the new year at December’s FOMC, finally easing off of a policy rate hovering at its highest in over two decades. As we will see, data throughout the quarter cut against that last theme, showing prices to be quite a bit stickier than policymakers were expecting, though equity markets shrugged off a relatively hawkish turn in the Fed’s tone by quarter’s end, closing markedly higher for the first three months of the year (Figure 1).

Figure 1: Equity Market Performance, Returns as of March 31, 2024

Source: S&P 500 (USD), FTSE All-Share (GBP), EURO STOXX 50 (EUR), MSCI Emerging Markets (USD), and CSI 300 (CNY), via Bloomberg.

Once again, US stocks were among the strongest performers globally, adding 10.6% in Q1 on the back of strong corporate earnings, with shares of the so-called “Magnificent 7” up over 17% for the quarter. Developed markets outside the US climbed by a respectable 5.8% in Q1, led by the world’s best-performing major market, Japan, whose Nikkei 225 index rallied 21.4% over the last three months, breaking the 40,000-yen mark for the first time ever and surpassing highs last hit in the late 1980s as wage growth, measured inflation, and signs of a return to expansion prompted the Bank of Japan to hike at its March meeting, finally putting an end to the nation’s negative-interest-rate policy. Emerging Markets gained a more modest 2.4% for the quarter, as concerns the Fed might delay easing weighed on economies generally more sensitive to US rates and dollar strength.

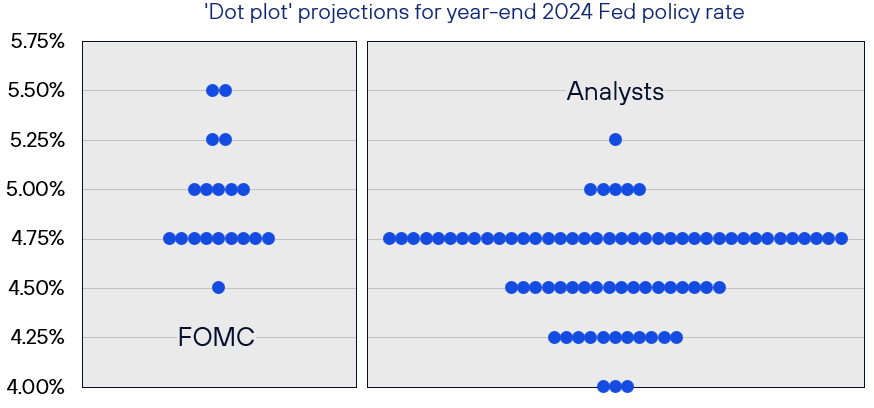

Of course, even US stocks should respond to changing expectations for the Fed’s policy path, and that is what we have typically observed over the last year or so, with markets often reacting strongly—and in the predicted direction—to not only Fed officials’ statements, but also evidence on consumer spending, updates on conditions in the labor market and, naturally, data on inflation. Especially with respect to the latter category, the last few months have been full of upside surprises, suggesting that disinflation has stalled somewhat since we entered the year, leading Fed chair Jay Powell and others at the central bank to back off earlier signaling of an imminent pivot to easing. As we have suggested before, it was never clear to us three cuts were a done deal for 2024, let alone the six cuts markets expected at the start of the year. In that sense, although we hoped for the best, it has been rather vindicating to see the consensus among professional forecasters move closer to our view (Figure 2), though investors’ optimism was such that stocks bucked the usual trend and rallied higher despite a steady increase in end-of-year predictions for the Fed funds rate (Figure 3).

Figure 2: Wall Street Still Seems More Dovish Than Fed Officials

The December FOMC brought with it a dovish pivot in Fed messaging, as the central bank’s heavily scrutinized “dot plots” showed a likely three rate cuts on the docket for 2024. Investors reacted by pricing in an even more bullish six cuts by year-end. Fast forward one quarter—with plenty of hot inflation data and what many perceived as a hawkish turn in Fed officials’ tone over the intervening three months—and the FOMC’s March revision to its rate forecast still showed a trio of cuts for 2024. We took the liberty of creating an equivalent dot plot for Wall Street analysts at the end of Q1, and while expectations have cooled off to a median three cuts, matching the Fed’s, we still see more optimism than we feel is warranted in a fatter tail on the dovish end of the distribution.

Source: Rayliant Research, FOMC, Bloomberg, as of March 25, 2024.

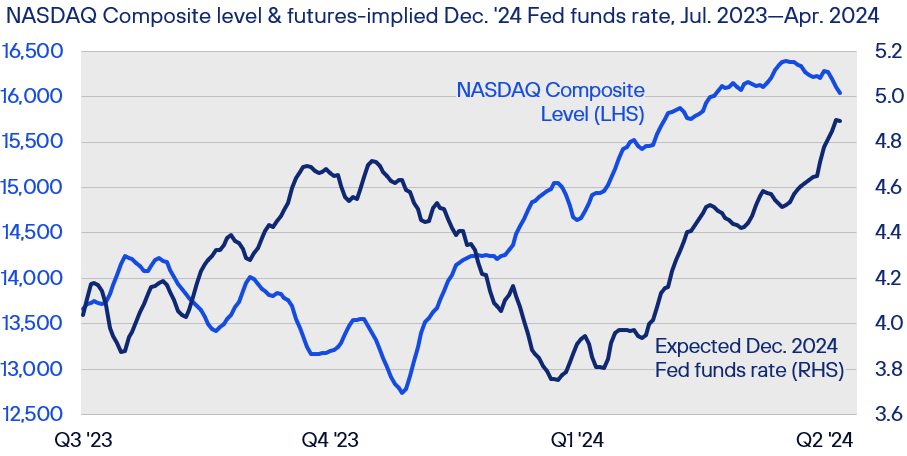

Figure 3: Rising Rate Expectations Couldn’t Stop “Risk-On” in Q1

Like many investors, we found ourselves in 2023 devouring macro data and hanging on Fed officials’ every word in search of clues as to Fed policy, which seemed to drive performance in every part of our asset allocation. Stocks often appeared just as reactive as bonds to any change in expectations for terminal policy rates, with shares rising on dovish data and falling at any hint of “higher-for-longer.” Oddly, despite mounting indications this year that a patient Fed will delay rate cuts in the face of sticky inflation, this familiar dynamic reversed at the start of Q1, with traders’ forecasts of the Fed funds rate at year-end marching higher in parallel with a rally in rate-sensitive equities on the NASDAQ composite.

Source: Rayliant Research, CME Group, as of April 17, 2024.

One story making the rounds at the end of the quarter was that stocks were rising because investors had rationally shifted attention from concern over the Fed’s timetable for easing to optimism that with the US economy running so hot and corporate earnings apparently robust, a likely soft landing justified relatively lofty valuations. Such a view explains why, at the end of Q1, professional money managers’ positioning in futures-based bets on a continuation of the S&P 500’s rally had reached record levels (Figure 4). We agree that growth is surprisingly strong, especially in light of how high rates have gotten since the Fed started hiking, and this is undoubtedly a positive for stocks.

Figure 4: Fund Managers’ Long Equity Bets Highest in Over a Decade

One way of quantifying money managers’ enthusiasm over U.S. stocks is by looking at the magnitude of bullish bets they’re making on the S&P 500 index. Data on trading in E-Mini futures on the S&P 500 index showed asset managers were net long to the tune of US$250 billion in early April, a record dollar amount of notional exposure. The S&P 500’s price has also made record highs this year, though it’s not just a surging index price pushing up the value of traders’ bets: Even when calculated as a percentage of total open interest, long positions in U.S. stock futures are higher than they’ve been since contrarian bargain-hunters swooped in amidst the global financial crisis (those same value investors would likely note that the S&P 500 costs over 3.6x more today than it did then).

Source: Rayliant Research, E-Mini S&P 500 Index futures contracts data via CME Group, CFTC, as of April 17, 2024.

On the flipside, we fear that today’s prices—especially in the case of US stocks, and particularly within the technology sector, where much of the last year’s gains are concentrated—already reflect the good news. Moreover, the longer rates stay high because the Fed isn’t comfortable with progress against inflation, the greater the risk that policymakers inadvertently overshoot, in our view, leading the tide to suddenly turn on that growth critical in supporting such valuations. That’s why in seeking exposure to stocks, we have increasingly tended toward markets outside the US, including emerging markets, which still present plenty of upside in the event a soft landing is realized, but meanwhile trade at much more forgiving multiples. It’s also why we lean heavily on our ability to actively manage our portfolios’ composition, selecting stocks for which we see higher quality and upside better balanced against risk. One risk to equities bubbling up at the end of Q1 was simmering tension in the Middle East threatening to boil over into a more disruptive conflict. While geopolitical conditions are certainly worth monitoring going into the second quarter, we note that investors sometimes focus too much on scary headlines at the risk of missing more substantive (albeit more mundane) sources of economic stress (Figure 5).

Figure 5: Geopolitical Fear Doesn’t Always Trigger to Market Stress

An investor following the headlines in the first quarter might easily have concluded geopolitical tensions posed just as great a threat to asset prices as delays in Fed easing. Indeed, with war still raging in the Ukraine and an Israel-Gaza conflict which seemed on the verge of spilling over into the broader Middle East, there were plenty of military hotspots for investors to sweat. Perhaps reassuringly, a comparison of geopolitical stress measured from a textual analysis of newsprint with equity volatility captured by the VIX shows only a weak connection between geopolitical conflict and financial stress. Though market anxiety spiked modestly around major geopolitical shocks, the biggest disturbances arose from things like the global financial crisis, the European debt crisis, and the pandemic.

Source: Rayliant Research, CBOE, Geopolitical Acts Index via D. Caldara & M. Iacoviello, as of March 31, 2024.

Fixed Income

After finishing 2023 with big fourth-quarter gains on a dovish change in the Fed’s posture, fixed income generally sold off in the first few months of the new year as central bankers walked back some of that optimism around a quick shift to a more accommodative stance (Figure 6). Consistent with greater perceived odds of a soft landing, riskier bonds—e.g., corporate credit, high yield, and emerging markets debt—enjoyed better relative returns.

Figure 6: Fixed Income Market Performance, Returns as of March 31, 2024

Source: ICE US Treasuries Core, FTSE Actuaries UK Conventional Gilts, S&P Int. Sov. ex-US, JPMorgan EMBI Global Core, iBoxx USD Liquid Inv. Grade, Markit-iBoxx GBP Liq. Corp., Bloomberg UK Gov. Inflation-Linked All Mat., expressed in USD, except for UK indices in GBP, via Bloomberg.

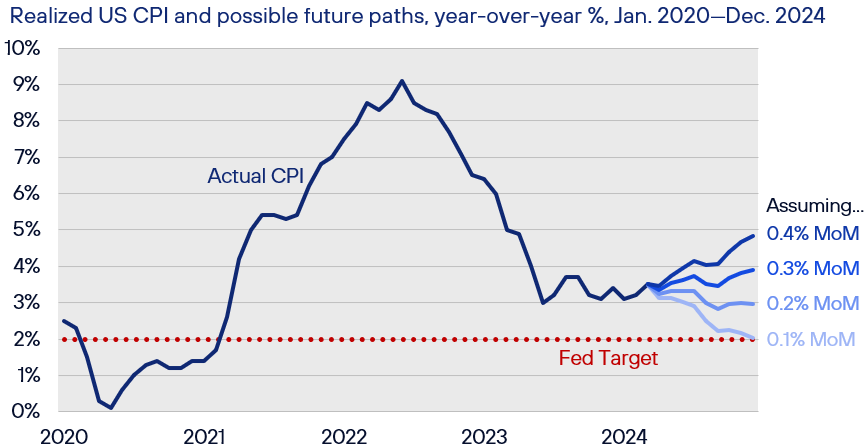

Inflation was once again squarely in focus, with pretty much every measure of rising prices we’re following showing a worrying stickiness over the first three months of 2024. The Fed, in turn, has gradually pushed a start to easing down its calendar, which becomes more problematic the closer we come to this fall’s US Presidential election. In fact, the Fed might not want to cut rates at that point, considering different scenarios for inflation leading into November, according to which last quarter’s trend puts headline CPI in the range of 4-5%, year-over-year (Figure 7). Our read is that the case for a June cut is almost a lost cause at this point, with one cut by year end seeming to us more likely, and zero cuts certainly conceivable depending on how inflation actually evolves.

Figure 7: Inflation Trending Higher Into November Elections

Although the Fed was founded as an independent agency on the hope its policymaking would be free of politicians’ influence, that doesn’t stop politicians from accusing the central bank of using its power to influence politics. Such perceptions put the Fed in a difficult spot, as the closer we come to the U.S. Presidential election in November, the harder it gets for the FOMC to begin its easing cycle without triggering claims those cuts are meant to impact the vote. Along these lines, we liked a back-of-the-envelope analysis by Bank of America recently, extrapolating various assumptions for month-over-month inflation into November. That work showed carrying forward a 0.4% monthly increase—merely the average rate observed in Q1—puts year-over-year CPI at 4.4% when voters hit the polls.

Source: Rayliant Research, Bank of America, Bureau of Labor Statistics, as of March 31, 2024.

Even if the US is not ready to make a move, the first quarter witnessed plenty of action happening in monetary policy across the rest of the developed and emerging world. Japan and Turkey were notable central banks hiking in Q1, though in the case of the former it was a bullish signal, while for the latter—whose policy rate ended March at a staggering 50%—it was a desperate attempt to contain inflation that clocked in at 68.5% year-over-year at the end of Q1. Overall, though, global central banks were clearly entering an easing cycle, with more banks lowering than raising rates as inflation has generally trended lower since the pandemic-era price increases that kicked off a massive wave of tightening in the last few years (Figure 8).

Figure 8: Despite Fed’s Hesitation, Central Banks Cutting in 2024

The Fed may be on the fence as to when it starts easing, but that hasn’t stopped many other central banks around the world from getting cuts underway. A look back at monetary policy cycles going back to the turn of the century shows just how much tightening there was to unwind at the beginning of 2024 after a wave of rate hikes starting in 2021, which aimed to crush pandemic-era inflation. Even as major advanced economies’ central banks debate when cuts might commence, many emerging economies—especially those in Latin America, a region with a history of dealing with inflation—had tightened sooner and were able to begin easing in the middle of last year. Whenever the Fed finally loosens up, they will likely be joining a chorus of cuts already in progress.

Source: Rayliant Research, Bank of International Settlements, NBER recessions shaded, as of March 31, 2024.

Outside of Turkey, that’s been the case in many emerging markets, and even a number of advanced economies like the Eurozone seemed poised to begin easing at some point in the second quarter. Of course, with so much focus on monetary policy, it’s easy to lose sight of the impact fiscal conditions can have on yields. Turning back to the US, it strikes us that investors’ anxiety about sustained deficits, especially unlikely to improve in an election year, could be another source of upward pressure on yields (Figure 9).

Figure 9: Little Progress Seen on US Fiscal Deficit This Decade

America’s fiscal deficit, the difference between the state’s spending and its income, totaled 8.8% of GDP in 2023, up from just 4.1% of GDP the year before, as the government shelled out 1.3 percentage points of GDP more at the same time tax revenues fell by 3.1 percentage points. Economists at the IMF recently warned the situation is unlikely to improve anytime soon, predicting an average fiscal deficit of 6.6% of GDP over the next six years and noting that the country’s “fiscal slippage”—especially around an election—poses a risk to both its domestic and the global economy. We see America’s fiscal irresponsibility as posing a risk to bond investors, as well, since Treasury issuance required to support excessive spending can only mean greater upward pressure on long-term yields.

Source: Rayliant Research, International Monetary Fund, as of April 17, 2024.

Alternatives

With the expected pace and magnitude of Fed rate cuts slipping throughout Q1, it was unsurprising to see real estate put in a modestly negative quarter, though the big story among alternative assets we’re tracking was in commodities, where a number of sectors were experiencing a pattern reminiscent of late-cycle outperformance sometimes witnessed in the space (Figure 10). Though a diversified basket of commodities was up a relatively modest 2.2% for the first three months of 2024, a handful of sectors posted remarkable outperformance to start the year.

Figure 10: Alternatives Performance, Returns as of March 31, 2024

Source: Bloomberg Commodity Index, Gold Spot, WTI Crude, iShares International Developed Real Estate ETF, all expressed in USD, via Bloomberg.

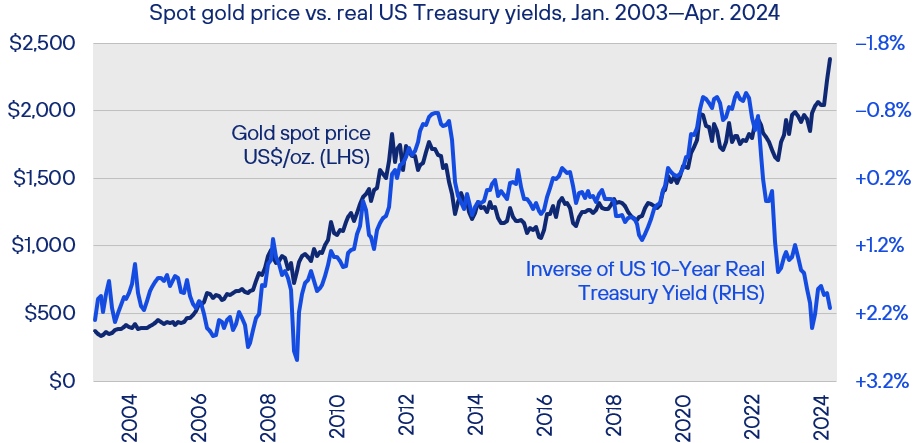

Precious metals were a case in point, with gold extended a sharp rally from the prior quarter on growing geopolitical concerns, big purchases by central banks around the world diversifying away from the US dollar, as well as anticipated Fed cuts that would reduce the non-yielding commodity’s negative carry. We find it notable that—similar to what we observed with growth stocks, whose typical inverse relationship to interest rates broke down amidst risk-on exuberance in Q1—gold traders seemed unfazed by rising yields (Figure 11), a potential sign of ‘overbought’ conditions to anyone considering a speculative bet on the rallying commodity.

Figure 11: Gold Investors Shrugging Off Rising Real Treasury Yields

The last few months have been spectacular for gold, with the precious metal hitting record highs as central banks stepped up purchases, diversifying away from the U.S. dollar—March marked a seventeenth straight month of net purchases by the People’s Bank of China—and investors sought a safe haven in light of fears conflict in the Middle East could quickly spiral out of control. That said, at least one catalyst for gold’s rally at the end of last year seems less relevant today: expectations for Fed rate cuts that would reduce the opportunity cost to holding an asset with no yield. In fact, we see the decoupling of gold’s price and real yields as a serious risk factor in a potential reversal of the commodity’s recent rally, especially if investors’ concerns geopolitical concerns wane in coming months.

Source: Rayliant Research, as of April 12, 2024.

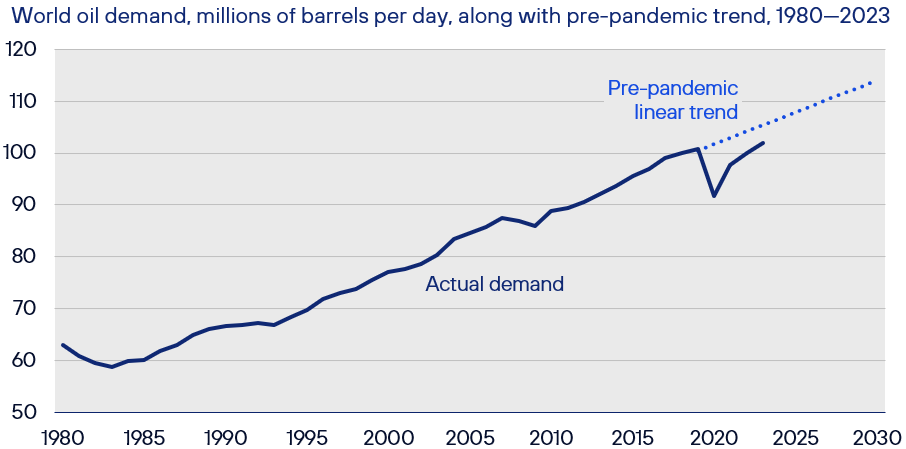

Another sector showing strength in the first quarter was energy, with the price of crude oil climbing by 15.7% through the end of Q1. Here we believe there’s a stronger fundamental case, as tight supply—resulting, in part, from voluntary production cuts by members of the OPEC+ group, initiated in 2022 and extended again in March—meets investors’ fear over disruptions related to Houthi attacks on Red Sea ships and potential broadening of conflict in the Middle East, as well as building optimism, on the other hand, that an economic soft landing will lead energy demand to further recover toward its pre-pandemic growth path (Figure 12). Though industrial metals were roughly flat for the first quarter, we see it as another sector where supply issues create great potential for outperformance in upside scenarios for the global economy, with China’s return to growth representing yet another catalyst that could push prices higher. Such thinking is the basis for the recent addition of metal mining shares to our diversified global models, where we believe valuations create a compelling entry point.

Figure 12: Crude Demand Still Tracks Short of Pre-Pandemic Trend

COVID-era restrictions on personal mobility and the disruption to energy prices from Russia’s invasion of Ukraine put a damper on oil demand in recent years which has only slowly recovered as the industry worked around issues with Russian supply and people across the globe got moving again post-pandemic. China loomed large on both sides of the shock to demand, with large-scale lockdowns of 2022 giving way to a 2023 re-opening, accounting for more than three-quarters of the bounce back in consumption for the year. Oil bears suggest the rise of EV and a broader new energy transition will keep oil demand from resuming its pre-pandemic trajectory. Even so, we think tight supplies, coupled with China’s return to growth and geopolitical factors could combine to keep prices high.

Source: Rayliant Research, US Energy Information Administration, trend calculated from 2000-2019.

Economic Calendar

Key Economic Releases and Events for 2024 Q2

United Kingdom

Bank of England Official Bank Rate Release: 9th May, 20th June

GDP Figures: 9th May, 27th June

PMI Figures: 1st May, 3rd June

CPI Figures: 21st May, 18th June

Eurozone

ECB Monetary Policy Meeting: 6th June

GDP Figures: 30th April

PMI Figures: 23rd April, 23rd May, 21st June

CPI Figures: 17th May, 18th June

United States

FOMC Rate Decision: 1st May, 12th June

GDP Figures: 25th April, 30th May, 27th June

PMI Figures: 1st May, 3rd June

CPI Figures: 15th May, 12th June

Important Information

The information contained in this article is the opinion of Henderson Rowe and does not represent investment advice. The value of investment may go up and down and investors may not get back what they invested. Past performance is not an indicator of future performance.

This document is intended for the use and distribution to all client types. It is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution would be unlawful and participation in the portfolio referred to herein shall not be offered or sold to any person where such sale would be unlawful. Any onward distribution of this factsheet is strictly prohibited.

The value of investments and the income from them can go up as well as down and you may realise less than the sum invested. Some investments may be subject to sudden and large falls in value and you may realise a large loss equal to the amount invested. Past performance is not an indicator of future performance. If you invest in currencies other than Sterling, the exchange rates may also have an adverse effect on the value of your investment independent of the performance of the company. International businesses can have complex currency exposure.

Nothing in this document constitutes investment, tax, legal or other advice by Henderson Rowe Limited. You should understand the risks associated with the investment strategy before making an investment decision to invest.

Investors should be aware of the risks associated with data sources and quantitative processes used in our investment management process. Errors may exist in data acquired from third-party vendors, the construction of model portfolios, and in coding related to the index and portfolio construction process. Information contained in this fact sheet is based on analysis of data and information obtained from third parties. Henderson Rowe Limited has not independently verified the third-party information. The firm, its directors, employees, or any of its associates, may either have, or have had, a position, holding or material interest in the investments concerned or a related investment.

Henderson Rowe is a registered trading name of Henderson Rowe Limited, which is authorised and regulated by the Financial Conduct Authority under Firm Reference Number 401809. It is a company registered in England and Wales under company number 04379340.