The beginning of the third quarter teased investors with yet another ‘bear market rally’, as stocks and bonds soared in July on a weaker-than-expected US CPI print, only to slide lower as Jerome Powell’s Fed increasingly signaled that one month of data would not count as sustained evidence of easing inflation. Instead, by quarter end, markets were pricing a ‘higher for longer’ policy orientation—including two jumbo rate hikes in Q3, amounting to 150 bps—which accounts for the abysmal performance of all major asset classes over the last three months. In our latest Quarterly Asset Class Update, we break this financial drama down by the numbers, offering thoughts as to where markets could be headed as 2022 heads into the home stretch.

Asset Classes

Equities

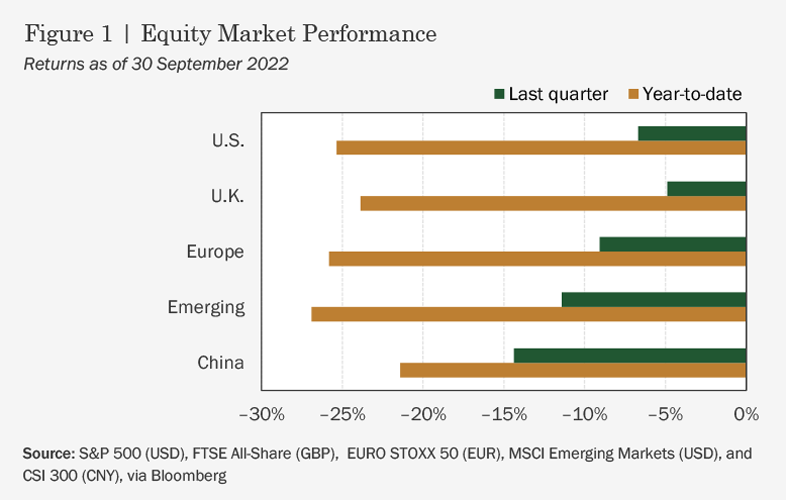

Investors hoping for good news near the end of August at an annual conference of central bankers in Jackson Hole, Wyoming were sadly disappointed when Fed Chair Jerome Powell reaffirmed the bank’s commitment to keeping rates high in its battle against inflation, predicting that hawkish policy required to tame rising prices would “bring some pain to households and businesses.” Markets, of course, are forward looking, and investors have been feeling the pain all year. A ‘bear rally’ in U.S. stocks that began at the end of the second quarter fizzled out shortly ahead of Powell’s Jackson Hole appearance, and equities sold off through the remainder of Q3 (see Figure 1). U.S. stocks lost –4.9% for the quarter, outperforming international equities, as developed markets outside of the U.S. fell by –9.1%. Emerging markets fared worst in Q3, falling by –11.4%, led down by Chinese stocks which, after posting the only positive return in the EM index for Q2, sank by –24.9% in the third quarter under damaging zero-COVID policies, domestic property market woes, and darkening prospects for the world economy.

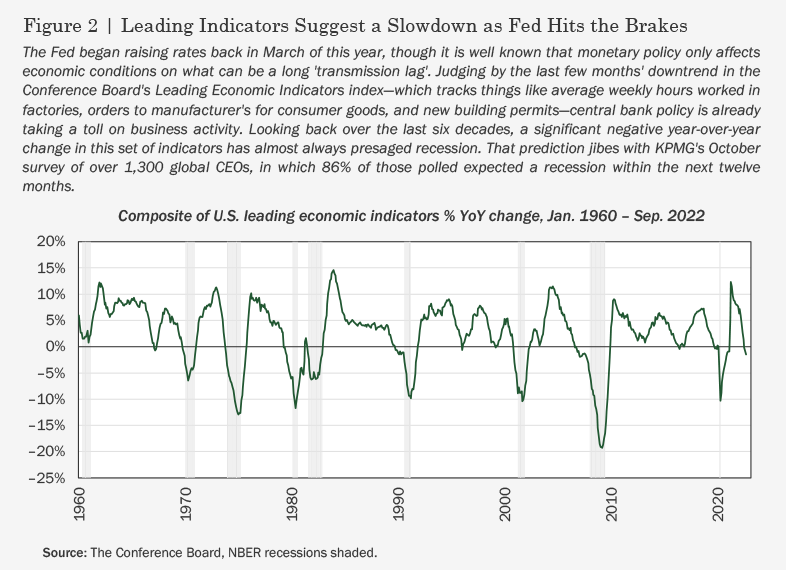

Stocks climbed from June to August largely on the basis of wishful thinking: a hope that central banks would see the sharp slowdown in economic growth and ‘hit pause’ on tightening, maybe even pivoting to an easing posture. By the end of September, however, it was quite clear that policymakers have accepted global recession, significant job loss, and falling asset values as a fair price to pay for keeping inflation in check, and that they see high interest rates over an extended period as the surest way to cool things down. In that respect, mounting signs of a serious economic contraction in the U.S.—which entered ‘technical’ recession in Q2, after consecutive quarters of negative GDP growth—might be taken as evidence that a rate hike cycle begun in March is finally having a real impact. This effect can be seen in the data, with the Conference Board’s Leading Economic Indicators index pointing to a sharp decline in economic activity (see Figure 2). It is also reflected in worsening sentiment among company insiders, including the 1,300+ CEOs recent polled by KPMG, 86% of whom expect a recession within the next year.

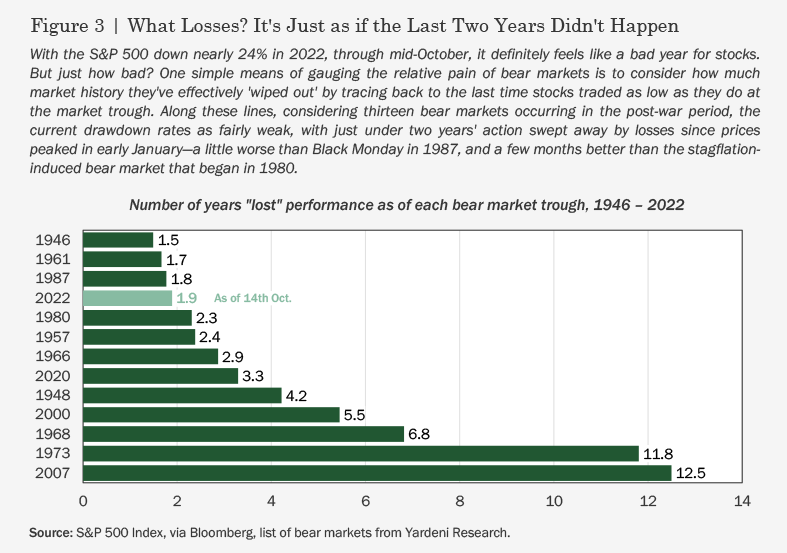

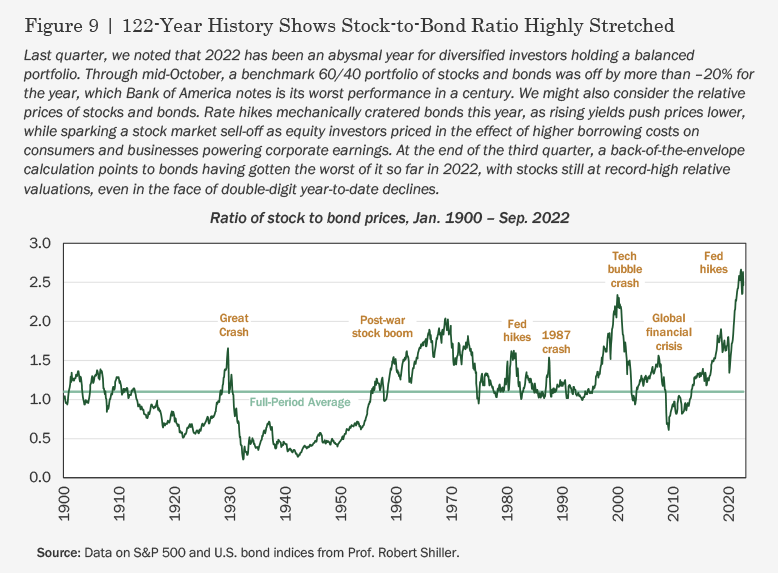

As of mid-October, waning sentiment on the part of investors had pushed U.S. stock valuations down by almost one-fourth, with equities deep in the throes of a bear market. Humans’ reaction to market moves is often anchored to our past experiences. As such, how one feels about the current equity rout depends on the market cycles one has lived through. With that in mind, measuring bear markets in terms of the time it took for the market to ‘giveth then taketh away’ investors’ paper gains, we find that the current drawdown—while certainly painful—has erased just about two years of market history, well better than average (see Figure 3). By contrast, losses in the market crash accompanying the Global Financial Crisis in 2007 and the meltdown in 1973 following Nixon’s ill-fated policies around Bretton Woods and the subsequent energy crisis were much more destructive in this sense, each ‘wasting’ around twelve years of investors’ time. Viewed from another perspective, a newcomer to investing whose sole experience of a bear market was the short-lived 2020 COVID crash, might fail to appreciate the impact a protracted decline could have on an equity investor’s wealth plan.

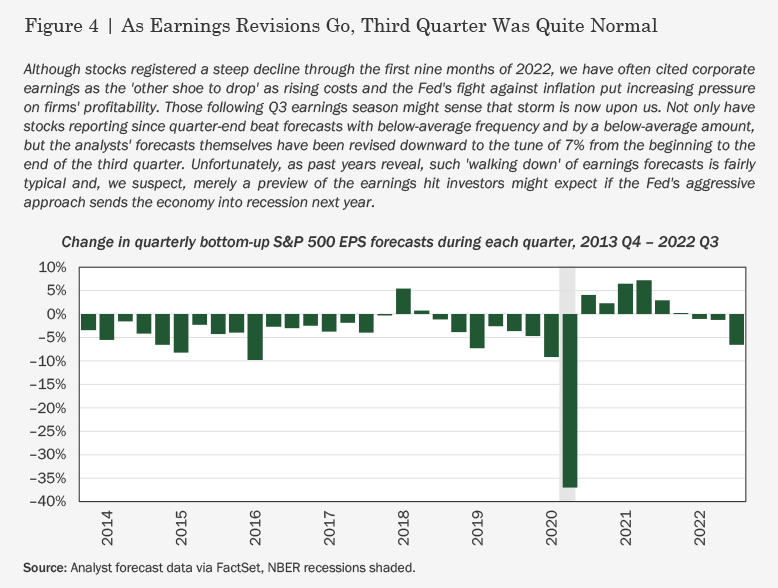

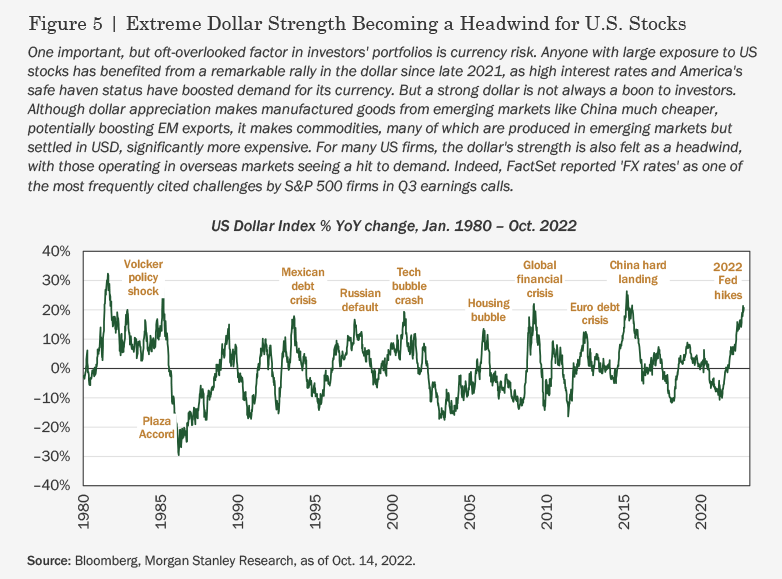

What could deepen and extend this year’s decline in stocks? As mentioned above, the primary aim of rate hikes is to combat inflation by slowing down activity in the economy—a result that cannot help but show up in softening corporate earnings. For those listening in to this quarter’s rather gloomy earnings calls and tracking the ensuing downward revisions in sell-side analyst forecasts, it might seem as if businesses are finally capitulating. In fact, past evidence suggests analysts’ shading of Q3 forecasts was actually just below par for the course (see Figure 4), and we expect to see profitability further squeezed before the Fed is satisfied and investors are safe to call a market bottom. Interestingly, one side effect of Fed rate hikes is U.S. currency strength (see Figure 5), as higher interest rates and a ‘flight to safety’ attract flows and boost demand for the dollar. This also weighs on U.S. companies’ earnings since American goods and services sold overseas become comparatively expensive. Morgan Stanley’s Chief U.S. Equity Strategist, Mike Wilson, recently noted that each 1% increase in the dollar’s strength reduces S&P 500 earnings by roughly –0.5%.

Fixed Income

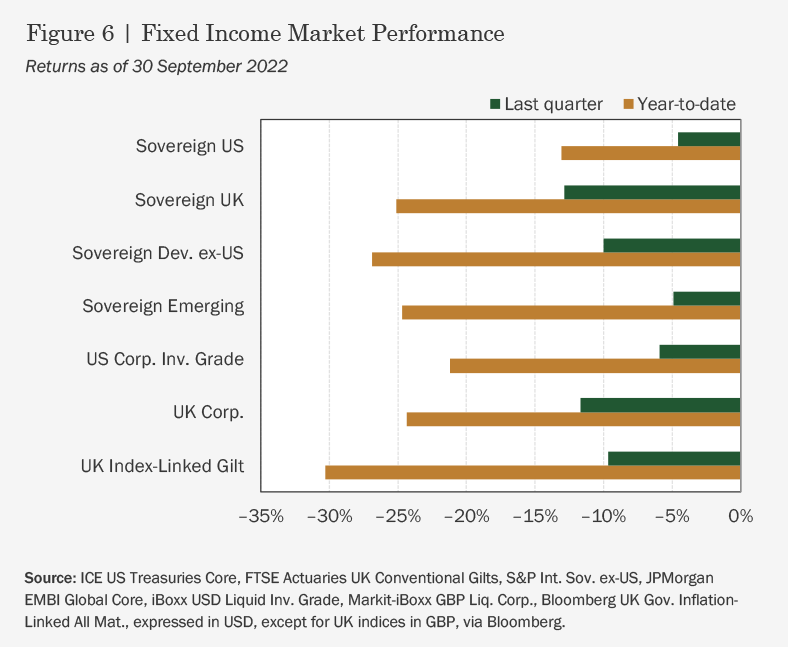

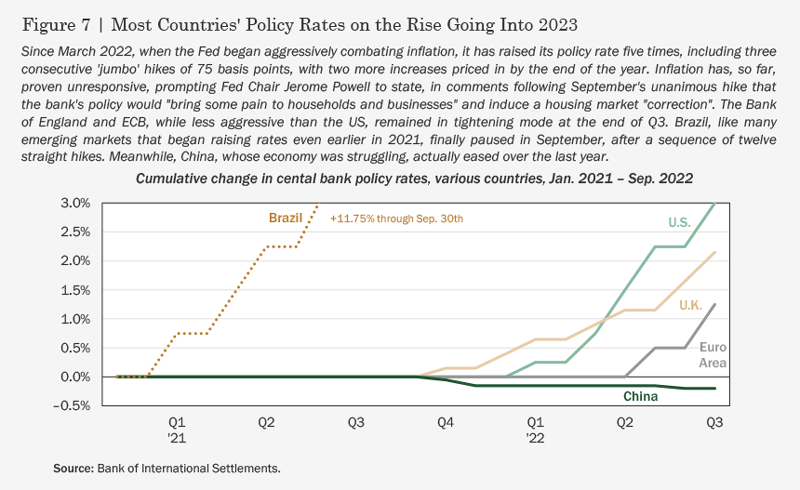

Restrictive monetary policy around the world continued to weigh on global bond returns in Q3, as all major segments of the fixed income market posted negative returns over the last three months, with Developed ex-U.S. sovereign issues faring worst, ending the quarter down roughly –10% (see Figure 6). A widely reported meltdown in the market for UK gilts in September accounts for part of the decline, as British government bonds suffered their worst one-day return since the March 2020 COVID crash in the wake of a disastrous ‘mini-budget’ announcement by new prime minister Liz Truss and her chancellor of Exchequer, Kwasi Kwarteng. The Conservative leaders promised massive and unfunded tax cuts and energy subsidies—apparently uncommunicated to the Bank of England—which spooked the market. The initial drop in gilt prices resulted in margin calls on UK defined-benefit pension funds, many of which use leverage to buy bonds for income and hedge volatility with derivatives, as large mark-to-market losses prompted brokers to demand more cash for collateral. Of course, To raise cash, funds were forced to sell gilts, which led to a vicious cycle in the gilt market, eventually prompting the Bank of England to step in and buy long-dated gilts to stabilize prices. Despite providing a bit of liquidity to stem a panic, England’s central bank, like its counterparts across many developed and emerging markets, was firmly in tightening mode throughout Q3 (see Figure 7).

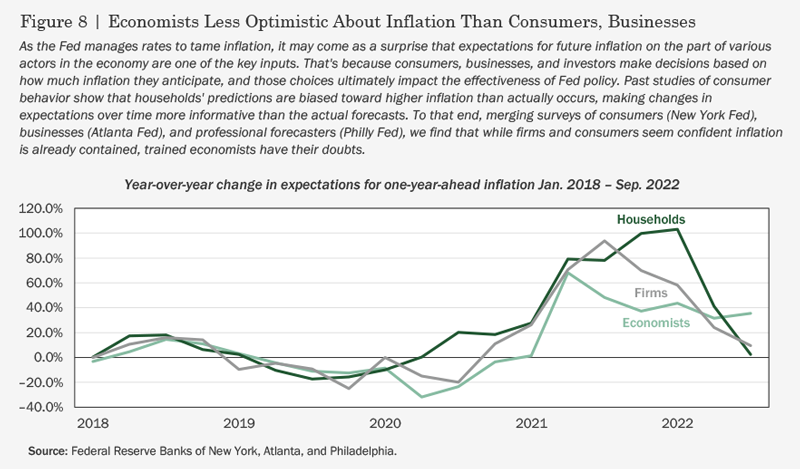

As mentioned before, such policy is clearly driven by a desire to alleviate inflationary pressures, which the Fed and other central banks believe represent a serious threat to the health of the world economy. What might be less obvious is that expectations for future inflation on the part of households and firms are a key input to bankers’ decisions about how exactly to use the monetary tools at their disposal in the fight against rising prices. For this reason, various branches of the Fed track inflation expectations among different groups over time, offering insights into how beliefs about the future course of prices are changing (see Figure 8). While consumers, businesses, and trained forecasters each registered increased concern over inflation in the wake of pandemic disruption—with households predictably overreacting relative to the professionals—the last few months have seen a marked decline in worry among consumers and firms about a continued climb in prices, suggesting many of those targeted by Fed policy underestimate the stickiness of inflation and may be disappointed when rates don’t soon revert. Judging by market prices, bond investors are paying closer attention to the comparatively bleak expert forecasts, having baked in a more pessimistic future than equity traders (see Figure 9).

Alternatives

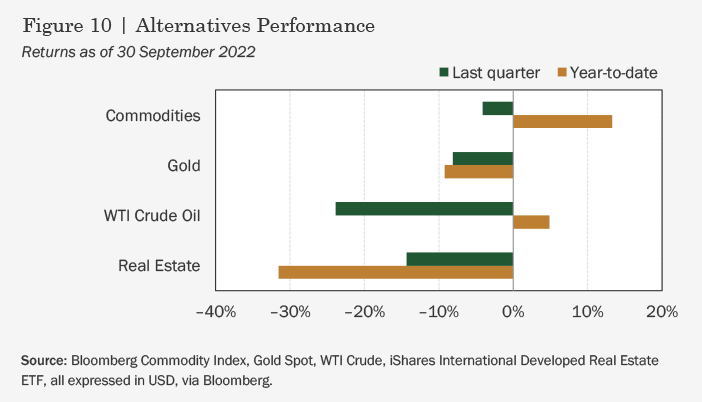

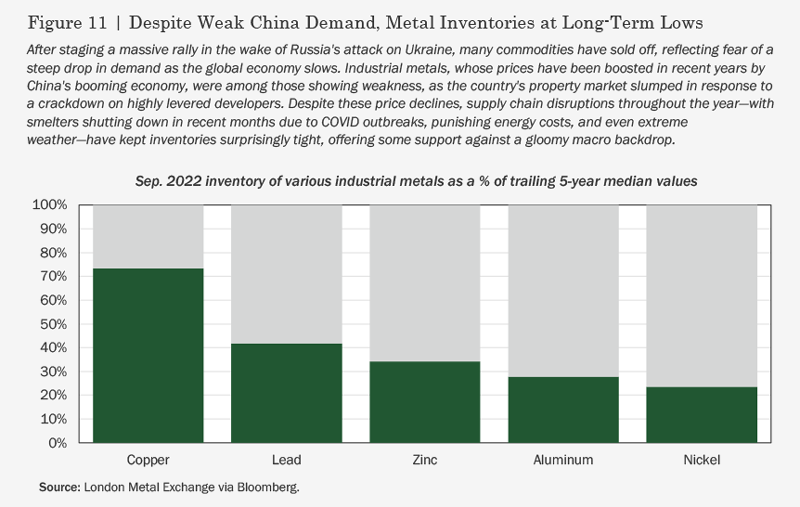

Recessionary fears spared few asset classes in Q3, as alternatives like commodities and real estate—often considered diversifying, relative to stocks and bonds, and a good hedge against inflation—sold off over the last three months (see Figure 10). Despite posting negative returns, commodities held up fairly well, shedding just –4.1%. Record-high natural gas prices offset weakness across much of the energy sector, climbing in response to Russian supply cuts, suspected sabotage of the Nord Stream undersea gas pipeline, and Europe’s impending winter season. Corn and wheat prices, still boosted by the Russia-Ukraine conflict, lifted agricultural commodities. Precious metals lost ground as a result of rising rates, which increase the opportunity cost to holding non-yielding assets, while industrial metals suffered from worries over the global economic downturn and its effect on demand. One factor limiting losses among industrial metals throughout the year has been the impact of supply chain disruptions, creating extremely tight inventories and ripe conditions for future price spikes in the event of any positive economic surprises out of China, by far such metals’ biggest consumer (see Figure 11).

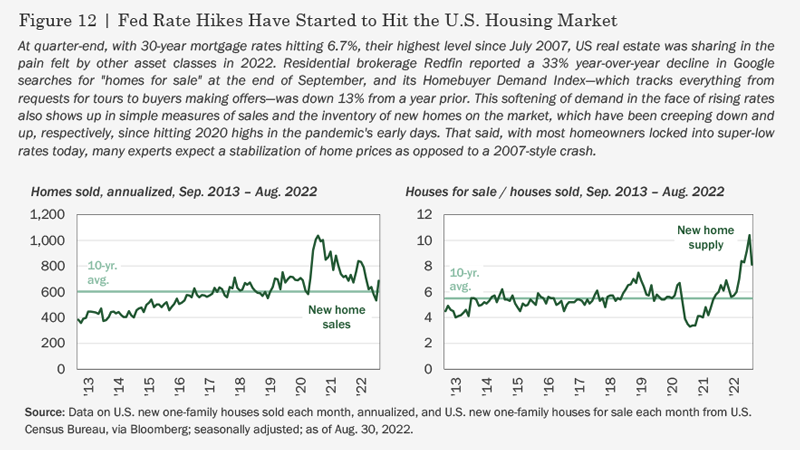

As mortgage rates climbed through the third quarter, some leading property market indicators began flashing signs of trouble in the U.S. real estate market. At the end of September, residential brokerage firm Redfin was tracking a meaningful decline in activity—including things like requests for tours and submitted offers—and reported that Google searches by homebuyers had fallen by a third over the last twelve months. Meanwhile, with Zillow reporting upward of 100% year-over-year increases in income required to afford a typical house in many major markets, new home sales have plummeted, and the inventory of unsold homes continues to rise (see Figure 12). Despite such gloomy statistics, with rates so low for such a long time, most homeowners were able to lock in extremely favorable terms, leading to much less risk of a housing market meltdown like that preceding the Global Financial Crisis. Instead, many pundits expect mortgage lenders and homebuilders to bear the brunt of a downturn, with residential real estate prices facing limited downside—but also considerably less growth than some homeowners have come to expect through the pandemic property boom.

Key Economic Releases & Events for Q4 2022

UNITED KINGDOM

Bank of England Official Bank Rate Release: 3rd November, 15th December

GDP Figures: 11th November, 22nd December

PMI Figures: 3rd November, 23rd November, 5th December

EUROZONE

ECB Monetary Policy Meeting: 15th December

GDP Figures: 5th November, 7th December

PMI Figures: 4th November, 23rd November, 1st December

UNITED STATES

FOMC Rate Decision: 2nd November, 14th December

GDP Figures: 30th November, 22nd December

PMI Figures: 1st November, 1st December

Core PCE Figures: 23rd December

IMPORTANT INFORMATION

This publication does not constitute a financial promotion as defined by Section 21 of the Financial Services and Markets Act 2000 (FSMA).

This document is intended for the use and distribution to all client types. It is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution would be unlawful and participation in the portfolio referred to herein shall not be offered or sold to any person where such sale would be unlawful. Any onward distribution of this factsheet is strictly prohibited.

The value of investments and the income from them can go up as well as down and you may realise less than the sum invested. Some investments may be subject to sudden and large falls in value and you may realise a large loss equal to the amount invested. Past performance is not an indicator of future performance. If you invest in currencies other than Sterling, the exchange rates may also have an adverse effect on the value of your investment independent of the performance of the company. International businesses can have complex currency exposure.

Nothing in this document constitutes investment, tax, legal or other advice by Henderson Rowe Limited. You should understand the risks associated with the investment strategy before making an investment decision to invest.

Investors should be aware of the risks associated with data sources and quantitative processes used in our investment management process. Errors may exist in data acquired from third-party vendors, the construction of model portfolios, and in coding related to the index and portfolio construction process. Information contained in this fact sheet is based on analysis of data and information obtained from third parties. Henderson Rowe Limited has not independently verified the third-party information. The firm, its directors, employees, or any of its associates, may either have, or have had, a position, holding or material interest in the investments concerned or a related investment.

Henderson Rowe is a registered trading name of Henderson Rowe Limited, which is authorised and regulated by the Financial Conduct Authority under Firm Reference Number 401809. It is a company registered in England and Wales under company number 04379340.