This article originally appeared on the Rayliant Global Advisors website. Click Here to view the original article.

On December 31, 2019, Chinese authorities first reported cases of a viral outbreak in Wuhan, Hubei Province, to the World Health Organization (WHO). In the nearly two months since then, the novel coronavirus, dubbed “Covid-19” and declared a Global Public Health Emergency, has infected more than 70,000 people in China and almost 30 other countries. Investors’ concerns over the cost of coronavirus to the global economy—which some estimates put at higher than US$100 billion—have made waves in global stock markets since the outbreak began.

Of course, not all investors are immune to the fear caused by deadly epidemics, and the market’s reaction need not be rational. In search of evidence of behavioral bias, Jason Hsu, Chairman and CIO at Rayliant Global Advisors and Head of Investment Solutions, Phillip Wool, examine the response of Chinese stocks to the current crisis, as well as strategies for profiting from such mistakes on the part of other traders. Studying an unusual feature of China’s market and novel data on the trades of foreign investors, their analysis reconstructs market movements in the weeks after the coronavirus emerged. The story they uncover is one of overreaction, contrarian trading, and the opportunities complicated events create in an inefficient, retail-driven market.

Coronavirus and Chinese Stocks: Your Drawdown Will Resume After the Break

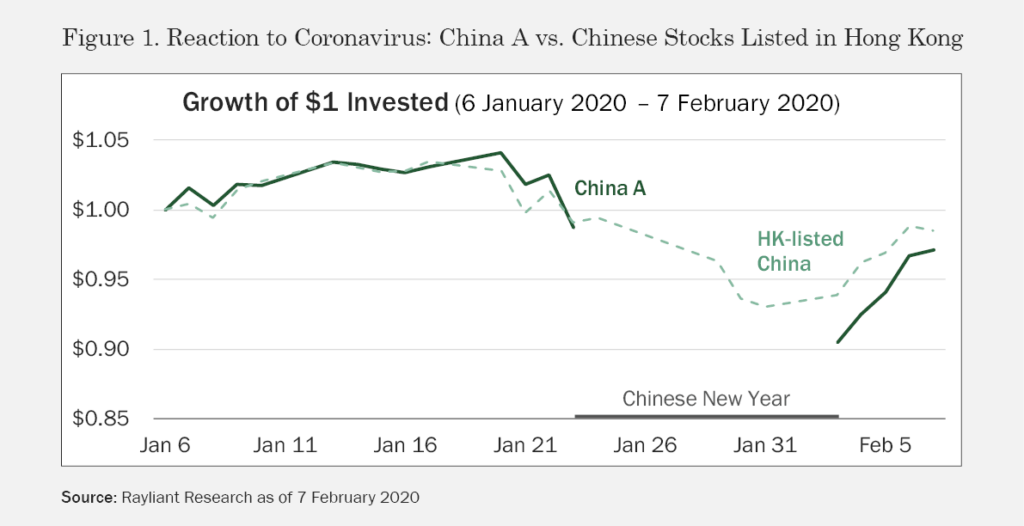

How did Chinese stocks react to developing news about coronavirus in January? In Figure 1, we track the value of $1 invested in a portfolio of mainland-listed Chinese stocks—the A shares traded in Shanghai (SHSE) and Shenzhen (SZSE)—beginning on January 6th, just before the coronavirus was identified by China and named by the WHO.

As reports revealed the outbreak’s severity increasing around mid-January, stocks traded in China were already beginning to dip. As a result of the Chinese New Year holiday, mainland stocks didn’t trade over the period from January 24th through February 2nd, which the Chinese authorities actually extended by three days in response to the outbreak. When A shares finally did open again on February 3rd, they ended the day 8% lower, the biggest hit since China’s bubble burst in 2015, wiping roughly US$400 billion off of the market’s value. Over 80% of all Chinese stocks reached their daily 10% downside limits, resulting in most of the market being suspended from trading by the end of the day. When the dust settled, mainland Chinese stocks had fallen by –10% since January 6th. In fact, mainland stocks only represent half of the story.

Chinese Companies Listed In Hong Kong: A Tale Of Two Markets

China’s market is interesting for many reasons, not least of which is the segmented nature of the country’s equity trading. We’ve been examining the A shares listed on China’s mainland exchanges, where over 80% of trading is done by individual non-professional investors. There is another set of Chinese stocks listed on the Hong Kong Stock Exchange (SEHK), where trading is dominated by sophisticated institutions. To be sure, these H shares, Red chips, and P chips are all mainland companies—they’re just traded in different places by different people. Figure 1 also depicts the value of $1 invested in Chinese stocks listed in Hong Kong since January 6th.

As we can see, HK-listed Chinese stocks moved in virtual lockstep with the A shares through January 23rd. While mainland stocks took a pause during the New Year break, Hong Kong’s market was open during most of this interval, and we can see Chinese companies listed on the SEHK sold off throughout the holiday period. That gave observers something close to a real-time indication of what to expect upon resumption of trading in A shares. Note that Chinese firms listed in Hong Kong bottomed out down around a –7% loss. Although both mainland and HK-listed stocks rebounded strongly in the days immediately following the A shares’ February 3rd rout, one week out, mainland stocks still lagged those listed in Hong Kong by about –1.4%.

The evidence so far suggests retail traders in China reacted somewhat more negatively to the outbreak than institutional investors in Hong Kong—and likely overreacted, given much of the gap was closed within a week. On the other hand, while onshore and offshore listings all represent Chinese companies, the exchanges differ in terms of which companies choose to list in each location. Hong Kong stocks have more weight on tech, for example, while manufacturing and consumer staples have more weight among A shares. It’s possible the markets reacted differently because they have differing economic exposure to the virus.

Running An Experiment On Dual-Listed Stocks

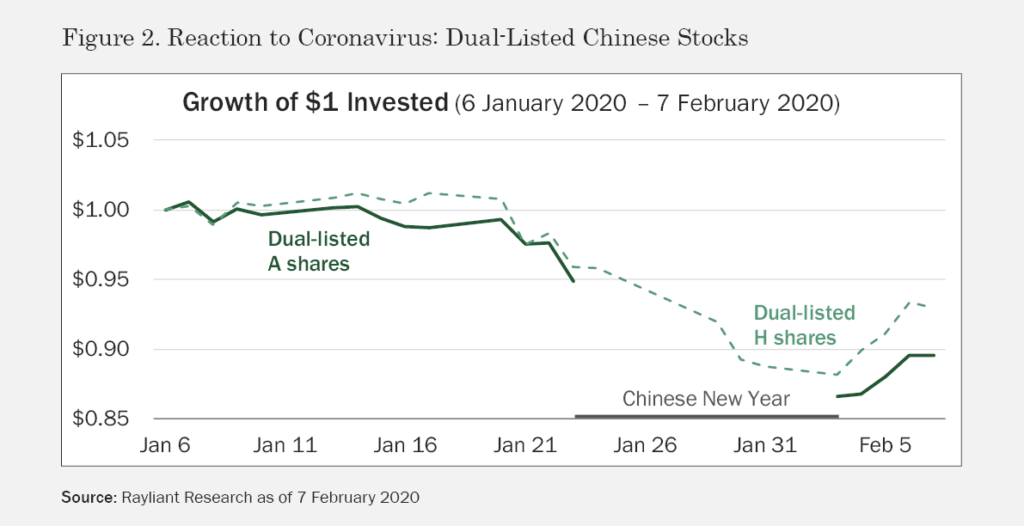

How might we address that concern? It turns out there exists an unusual set of Chinese companies that cut to the core of our question. As of January 6th, there were 111 dual-listed firms with A shares listed on the Shanghai or Shenzhen exchange and corresponding H shares listed in Hong Kong. Both share classes offer investors the exact same voting rights and dividend rights—they simply trade in different markets. Comparing the reaction of shares in the same company listed in two places gives us a much cleaner test for differences in the reaction of investors in each market to the same piece of news. In Figure 2, we track the value of $1 invested on January 6th for pairs of A and H shares.

We observe a very similar pattern to what we saw before, with the A shares reacting more negatively to news of the 2019-nCov outbreak and recouping some of their losses in the days subsequent to Chinese New Year. The average difference in returns for dual-listed stocks was still –3.4% by February 7th, indicating a greater degree of negative sentiment on the part of mainland investors. This is our best evidence yet that the prices of Chinese stocks are greatly affected by who trades them, with retail investors potentially overreacting to bad news. But does that have any implications for professional investors’ portfolios?

Following the “Smart Money” On Stock Connect

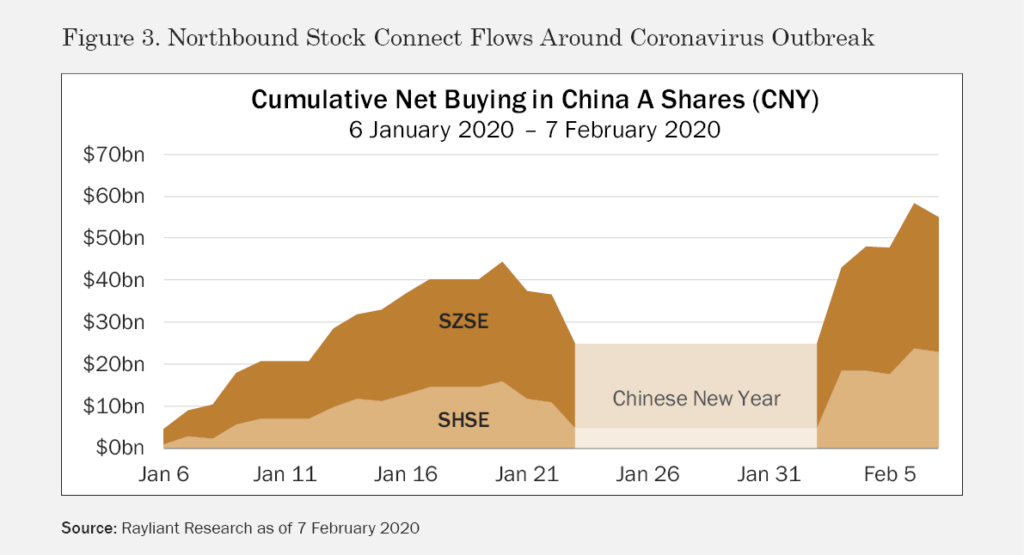

To understand the aftermath of the A shares’ selloff, we collected data on daily flows in and out of mainland stocks over the Northbound Stock Connect trading platform, which allows professional offshore investors to easily access A shares. In Figure 3, we plot cumulative net buying over the same period examined before to see how foreign institutions reacted to coronavirus news in their trading of mainland stocks.

In the first half of January, we see foreign investors’ allocation to A shares steadily climbing. But as concern over the outbreak mounted in the middle of the month, not wanting to hold equity risk through an extended market closure, Stock Connect traders sharply reduced exposure to mainland stocks ahead of the Chinese New Year. When stocks finally resumed trading on February 3rd, rather than selling into the downturn, foreign investors actually bought US$2.6 billion in mainland shares at a hefty discount to pre-holiday valuations. Those trades were clearly rewarded as A shares rallied over the next week. This pattern is consistent with our previous research documenting Northbound Connect traders as “smart money” in China’s mainland market, profitably taking the other side of retail investors’ trades.

Closing Thoughts

We’ve tracked market reactions to an epidemiological event across Chinese stocks traded in different places by very different groups of investors. We saw that retail investors punished mainland stocks more harshly than their institutional counterparts in Hong Kong as fears over the coronavirus increased, leading to a substantial divergence in prices between A shares and H shares trading on the same firm. Only time will truly tell whether mainland or Hong Kong investors’ response was “correct”—hindsight is always 20/20—but that didn’t stop offshore institutions from placing timely bets on a recovery in A shares after mainland markets’ February 3rd nosedive. One thing is certain: Features like trading suspensions, dual listings, and Stock Connect traffic make China’s market more complicated, but they also make analyzing the action in A shares much richer and create profound opportunities for investors with a local edge and the data to put that advantage to work.

IMPORTANT INFORMATION

This document does not constitute a financial promotion under Section 21 of the Financial Services and Markets Act 2000 (‘FSMA’). Henderson Rowe is a registered trading name of Henderson Rowe Limited, which is authorised and regulated by the Financial Conduct Authority under Firm Reference Number 401809. Investing with Henderson Rowe or any other investment firm involves risks. Please ensure that you fully understand the risks before investing. The value of investments may go up as well as down and you may not get back the amount invested. Past performance is not an indicator of future performance.

The content of this article represents the writer’s own view. Nothing in this article constitutes investment, tax or legal advice.