Market Overview

Investors will remember the beginning of 2020 for a long time. Regardless of how the situation unfolds the rest of the year, we know that most of us have not seen such volatile markets for a very long time. In fact, for those who started investing after 2008, this is the first experience with a bear market. Back in March, the market signalled that the global economy was on the brink and a liquidity crisis threatened an avalanche of insolvencies and bankruptcies. Central banks stepped in quickly, boosting and maintaining liquidity in Treasury and corporate bond markets. This support, combined with a range of coordinated fiscal stimuli around the globe, allowed the markets to find the bottom and stage one of the sharpest short-term rallies in history.

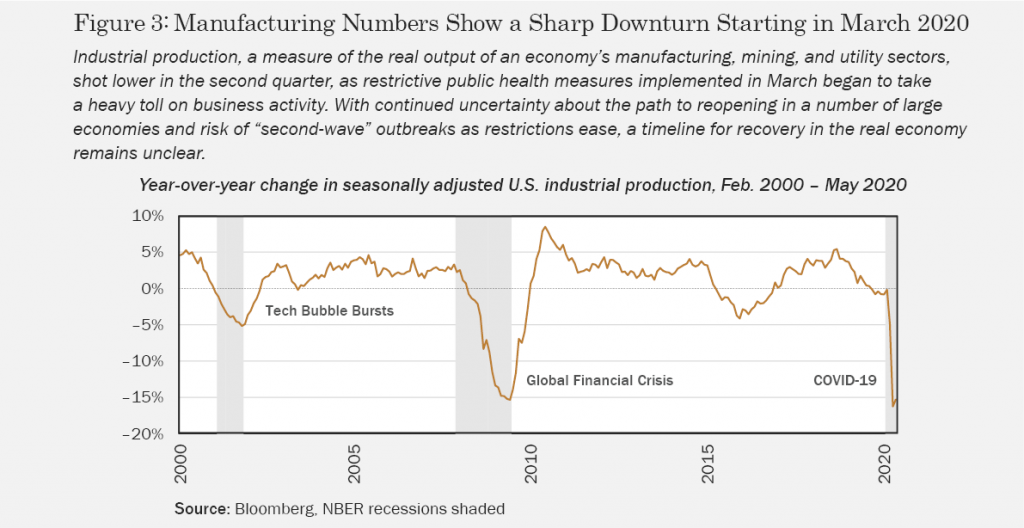

Taking the behaviour of stock markets as an economic indicator, one might get the impression that the world economy is in a good place right now. Unfortunately, it is the exact opposite. The global economy today finds itself in a crisis not yet witnessed in the 21st century. US unemployment increased from 4% to 14% in just under two months, and the UK’s real picture is likely to emerge after the end of the furlough program in September, but already expected to come in at close to 15%. All developed countries have implemented various fiscal stimulus programs aimed at maintaining consumption. Still, it is difficult to say what the long-term effects of these measures will be and whether consumer appetites for spending can return to pre-crisis levels. Only time will tell. For now, the market—or at least the technology sector—tells a positive story.

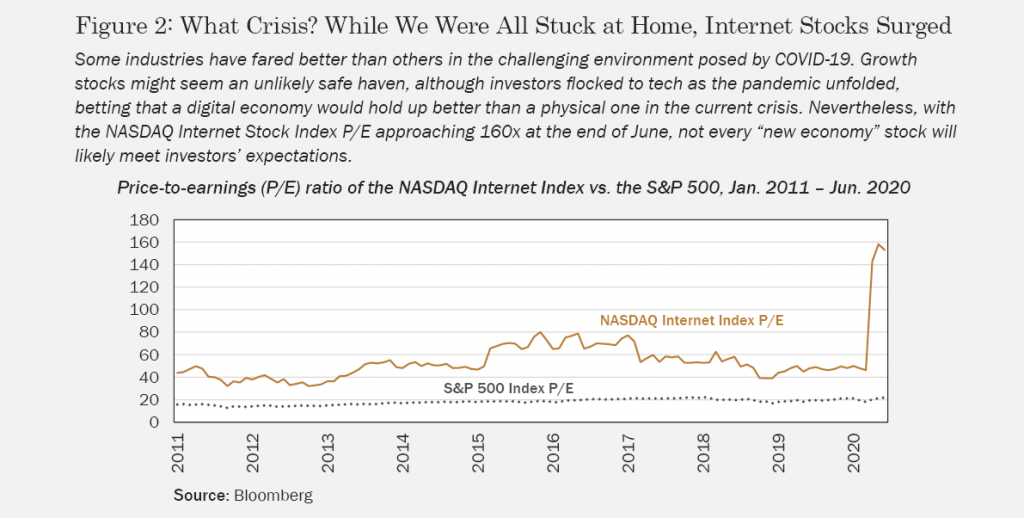

One of the most critical consequences of the COVID crisis is an acceleration of the automation—or, as it has been called, the “de-humanisation”—of the corporate world. Fewer humans means higher margins, limited pension liabilities and almost perfect resource efficiency. The software sector seems to be the only one that matters, and it has infiltrated nearly every industry on the planet. E-commerce, autos, TV, education and even farming rely on some software and, more importantly, require less human input. No wonder NASDAQ is up 17% year to date, and almost 40% since its March lows. Everyone wants to be on the tech bandwagon.

Sharp stock market rallies have a unique tendency to create a gambling mentality in retail investors’ minds. The Tech Bubble, Global Financial Crisis and the Bitcoin rally in 2018 all share one similar feature: retail investors piling in at the top. High levels of greed usually lead to “this time is different” thinking. New valuation tools, often not based on cash flows, are introduced by market participants to justify buying overvalued stocks. Reasons given as to why markets and businesses have changed are often based on farfetched narratives. Nevertheless, as more and more retail investors make more and more money, the mania continues. Every day the market rallies, remaining critics are proven wrong and not participating in the bubble becomes psychologically and financially painful. Everyone hopes they will sell at the top, but history tells us few will manage to do so.

This isn’t to say the world is in a bubble, though certain corners of the market are beginning to flash “bubble-like” characteristics that should concern us. Big tech’s growth is robust, to be sure, and its long-term prospects are promising. For many software businesses, the pandemic is undoubtedly a game-changer, forcing consumers to embrace an “online” way of life. Speculation these days tends to appear in single names or subsectors. Cannabis stocks, new-era auto stocks, single-product companies—the list is long. Every good analyst knows that a stock’s price reflects a mix of its discounted cash flow valuation and the optionality of selling it to someone else at a higher price. Our job is to find the ones that are a mix of both and avoid the ones trading purely on the latter: so-called “narrative stocks”. Should an auto manufacturing company which has a negative cash flow and less than 1% of global sector revenues trade higher than all other auto manufacturers combined, implying decades of near-monopoly? Maybe, but with fundamentals saying otherwise current shareholders are betting on the greater fool theory.

There is nothing wrong with speculating on one’s own account. As long as one understands the risk, doesn’t speculate with most of one’s savings and knows speculation is not investment, losses should be limited. The problem starts when the greater fool theory begins to dominate investment decision making, and one’s main portfolio moves away from a well-diversified selection of investments towards a handful of stocks picked based on charismatic CEOs and sexy narratives. As the world struggles under the weight of a pandemic and the company’s shares are at an all-time high, that charismatic CEO you were so excited about is already working on the exit strategy…are you?